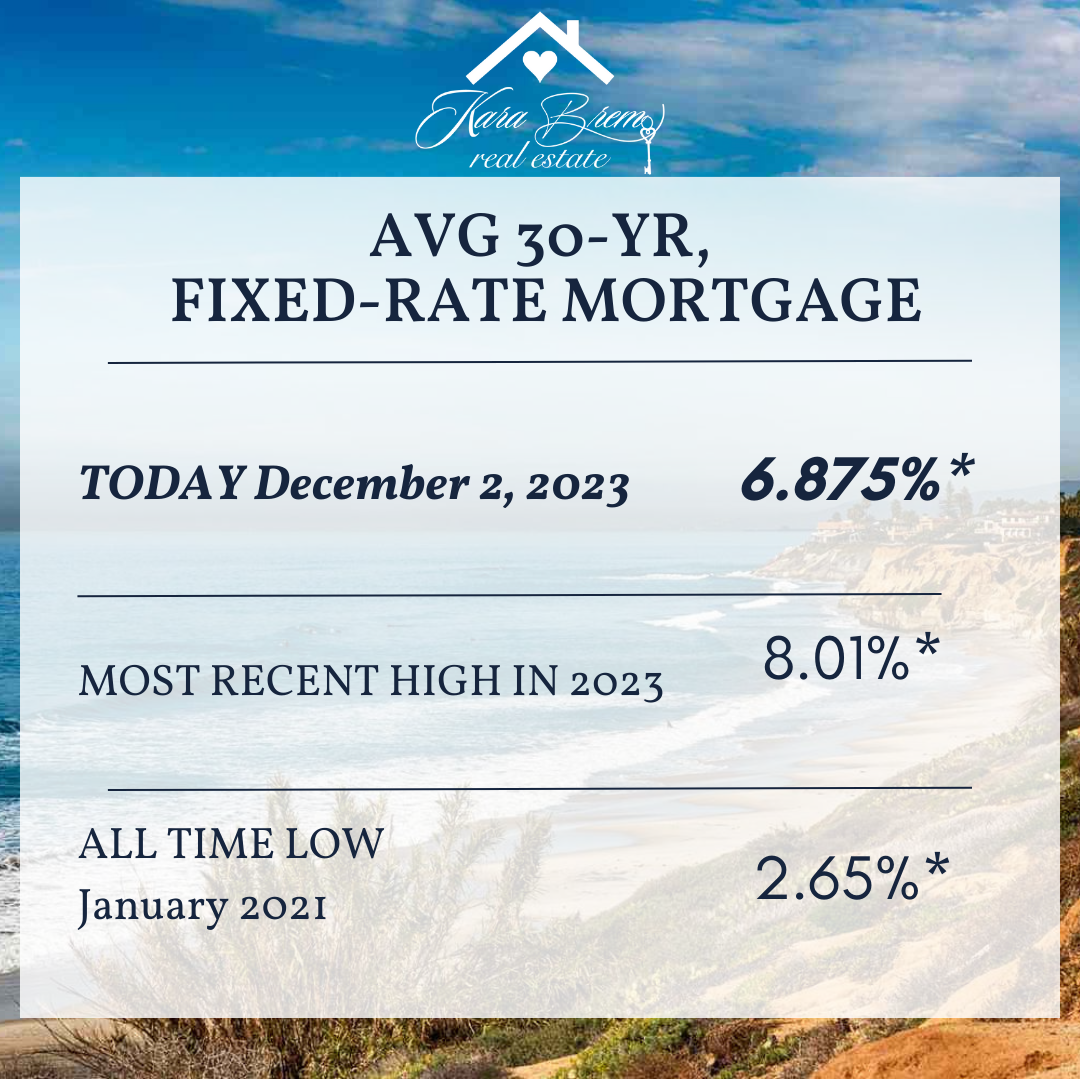

The holiday season is delivering early gifts to would-be buyers.

Having climbed relentlessly for most of 2023, from just below 6% to just over 8%, average 30 year mortgage rates have plummeted in recent weeks to mid 6’s. Woohoo! Furthermore, with inflation continuing to trend lower, the markets are increasingly convinced that the Fed it’s done hiking rates and could start CUTTING rates in the first half of 2024.

Other big news is the new loan limits for 2024. In San Diego County, the Conventional limit is up to $766,550 and the high loan limit is up to $1,006,250. Most lenders begin using these new limits right away.

It’s beginning to look a lot like Christmas. 🙂

*No points purchased. Rates are based on 30 year fixed with excellent credit score and 20% down. This is just an estimate. Rates may vary.

.

.

.

Kara Brem REALTOR®

DRE Lic. #01939667

(831) 818-3050

kara@karabrem.com

This past year, rising mortgage rates have slowed the red-hot housing market. Over the past nine months, we’ve seen fewer homes sold than the previous month as home price growth has slowed. All of this is due to the fact that the average 30-year fixed mortgage rate has doubled this year, severely limiting homebuying power for consumers. And, this month, the average rate for financing a home briefly rose over 7% before coming back down into the high 6% range. But we’re starting to see a hint of what mortgage interest rates could look like next year.

Inflation Is the Enemy of Long-Term Interest Rates

As long as inflation is high, we’ll see higher mortgage rates. Over the past couple of weeks, we’ve seen indications that inflation may be cooling, giving us a glimpse into what may happen in the future. The mortgage market is eagerly awaiting positive news on inflation. As Ali Wolf, Chief Economist at Zonda, says:

“The housing market is expected to face continued uncertainty heading into 2023 as consumers, financial markets, and policymakers work through their respective challenges in today’s economy. . . . we are watching for any additional stability in the MBS market, signs of cooling inflation, and/or less aggressive Federal Reserve action to give us confidence that mortgage rates are past their peak.”

What Does This Mean for the Future of Mortgage Rates?

As we get through the inflation battle and start to see that coming down, we should expect mortgage rates to follow. We’ve seen nods of this over the past couple of weeks. As the Federal Reserve works to bring inflation down, mortgage rates will come down as well. Bill McBride from Calculated Risksays:

“My current view is inflation will ease quicker than the Fed currently expects.”

As we look toward next year, we certainly hope he’s right.

Bottom Line

Mortgage rates will come down – it’s just a matter of time. The hope is we continue to see more positive news on inflation, and that’ll bring mortgage rates down. This will give prospective homebuyers more buying power and lead to more homeowners throughout the country.

Many consumers are wondering what will happen with home values over the next few years. Some are concerned that the recent run-up in home prices will lead to a situation similar to the housing crash 15 years ago.

However, experts say the market is totally different today. For example, Odeta Kushi, Deputy Chief Economist at First American,tweeted just last week on this issue:

“. . . We do need price appreciation to slow today (it’s not sustainable over the long run) but high price growth today is supported by fundamentals- short supply, lower rates & demographic demand. And we are in a much different & safer space: better credit quality, low DTI [Debt-To-Income] & tons of equity. Hence, a crash in prices is very unlikely.”

Price appreciation will slow from the double-digit levels the market has seen over the last two years. However, experts believe home values will not depreciate (where a home would lose value).

To this point, Pulsenomics just released the latest Home Price Expectation Survey – a survey of a national panel of over 100 economists, real estate experts, and investment and market strategists. Itforecasts home prices will continue appreciating over the next five years. Below are the expected year-over-year rates of home price appreciation based on the average of all 100+ projections:

2022: 9%

2023: 4.74%

2024: 3.67%

2025: 3.41%

2026: 3.57%

Those responding to the survey believe home price appreciation will still be relatively high this year (though half of what it was last year), and then return to more normal levels over the next four years.

What Does This Mean for You as a Buyer?

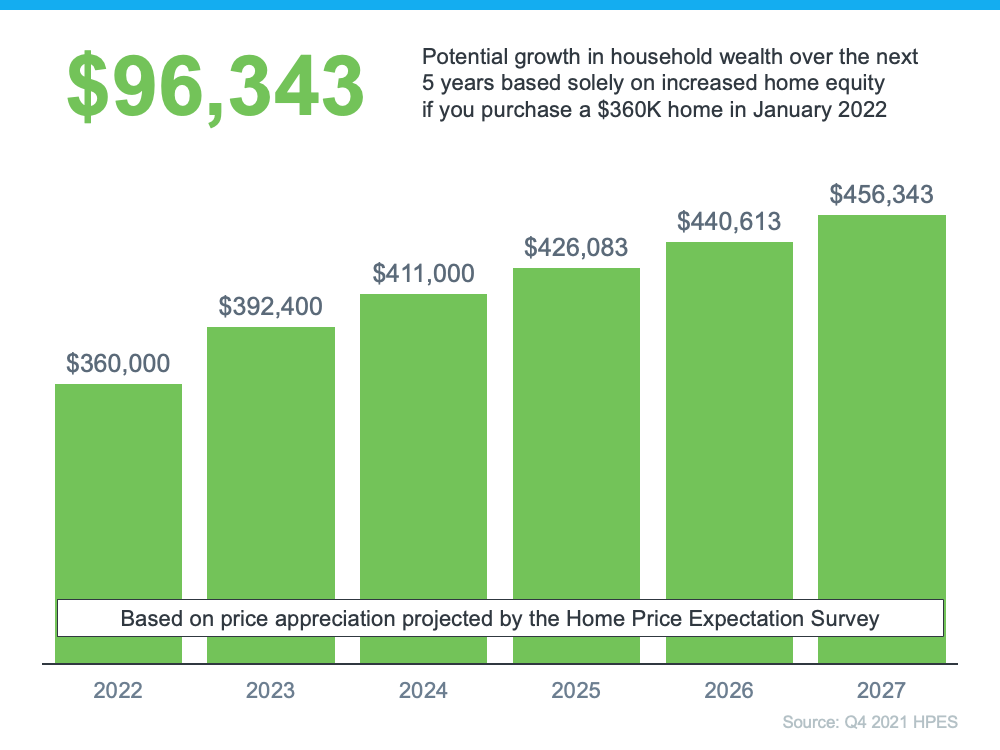

With a limited supply of homes available for sale and both prices and mortgage rates increasing, it can be a challenging market to navigate as a buyer. But buying a home sooner rather than later does have its benefits. If you wait to buy, you’ll pay more in the future. However, if you buy now, you’ll actually be in the position to make future price increases work for you. Once you buy, those rising home prices will help you build your home’s value, and by extension, your own household wealth through home equity.

As an example, let’s assume you purchased a $360,000 home in January of this year (the median price according to the National Association of Realtors rounded up to the nearest $10K). If you factor in the forecast for appreciation from the Home Price Expectation Survey, you could accumulate over $96,000 in household wealth over the next five years (see graph below):

Bottom Line

If you’re trying to decide whether to buy now or wait, the key is knowing what’s expected to happen with home prices. Experts say prices will continue to climb in the years ahead, just at a slower pace. So, if you’re ready to buy, doing so now may be your best bet for your wallet. It’ll also give you the chance to use the future home price appreciation to build your own net worth through rising equity. If you want to get started, let’s connect today.

Interest rates for a 30-year fixed rate mortgage have been on the decline since November, now reaching lows last seen in January 2018. According to Freddie Mac’s latest Primary Mortgage Market Survey, rates came in at 4.12% last week!

This is great news for anyone who is planning on buying a home this spring! Freddie Mac had this to say,

“Mortgage interest rates have been steadily declining since the start of 2019. These lower mortgage interest rates combined with a strong labor market should attract prospective homebuyers this spring and could help the housing sector regain its momentum later in the year.”

To put the low rates in perspective, the average for 2018 was 4.6%! The chart below shows the recent drop, and also shows where the experts at Freddie Mac believe rates will be by the end of 2019.

Bottom Line

If you plan on buying a home this year, let’s get together to start your home search to ensure you can lock in these historically low rates today!

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link