If you have student loans and want to buy a home, you might have questions about how your debt affects your plans. Do you have to wait until you’ve paid off those loans before you can buy your first home? Or is it possible you could still qualify for a home loan even with that debt? Here’s a look at the latest information so you have the answers you need.

“Roughly 60 percent of U.S. adults who have held student loan debt have put off making important financial decisions due to that debt . . . For Gen Z and millennial borrowers alone, that number rises to 70 percent.”

This includes one of the biggest financial decisions you’ll ever make, buying a home. But you should know, even with student loans, waiting to buy a home may not be necessary. While everyone’s situation is unique, your goal may be more within your reach than you realize. Here’s why.

Can You Qualify for a Home Loan if You Have Student Loans?

According to an annual report from the National Association of Realtors (NAR), 38% of first-time buyers had student loan debt and the typical amount was $30,000.

That means other people in a similar situation were able to qualify for and buy a home even though they also had student loans. And you may be able to do the same, especially if you have a steady source of income. As an article from Bankratesays:

“. . . you can have student loans and a mortgage at the same time. . . . If you have student loans and want a mortgage, there are multiple home loan programs you might qualify for . . .”

The key takeaway is, for many people, homeownership is achievable even with student loans.

You don’t have to figure this out on your own. The best way to make a decision about your goals and next steps is to talk to the professionals. A trusted lender can walk you through your options based on your situation, and share what’s worked for other buyers.

Bottom Line

Lots of other people with student loan debt are able to buy their own homes. Talk to a lender to go over your options and see how close you are to reaching your goal.

Existing-home sales across the US rose in December climbing 0.8% from the previous month and breaking a five-month streak in which sales declined, according to the National Association of REALTORS® (NAR).

Despite the increase, sales were down compared to the same period last year, as affordability challenges continued to hinder prospective buyers. Most of this period’s closed sales went under contract in October, when mortgage rates were at a two-decade high.

With rates having dropped more than a full percentage point since then, existing-home sales are forecasted to pick up in the coming months.

With average, 30-yr mortgage rates DROPPING, and inflation abating, the outlook for 2024 is positive. That being said, homebuyer demand is picking up, and without a significant increase in supply, experts believe home prices will likely remain elevated for some time to come.

NOTE: There are two photos. One is for detached homes in North county, SD and the other is for attached (condos and townhomes). If you would like specific cities or zip codes reach out to me for a more tailored synopsis.

Every buyer and seller’s situation is different and personal. Is it the right time for you to buy or list your property? Give me a call and let’s assess together. I will provide you accurate and relevant data so you can make the most informed decision possible.

The interior design trends of 2022 included a renaissance of colorful decorating, a preference for sustainable materials, and incorporating nature throughout the home. They reflected the continued evolution of our lifestyles in recent years and showed an overall desire for our homes to be somewhere we can relax, decompress, and focus on our wellbeing.

With 2023 just around the corner, expect to see the latest design trends continue that trajectory of creating a home that’s vibrant yet soothing.

5 Interior Design Trends for 2023

1. Butler’s Pantries

There’s something endlessly fascinating about features throughout a home that tie spaces together and create harmony. A butler’s pantry is the perfect resource for homeowners who feel their kitchens are always running at capacity. Typically located adjacent to the kitchen or dining room, modern butler’s pantries are often concealed behind cabinets or pocket doors. An economical solution for food and kitchen item storage, they allow you to prep meals outside the kitchen, gather silverware, and prepare to set the table. Kitchens are the heart of the home, and this space has taken on even more significance in recent years. It’s no wonder these special home features are on the rise.

Image Source: Getty Images – Image Credit: PC Photography

2. Colorful Kitchens

Color in the kitchen is back in style! The neutral-toned backdrop of farmhouse-style interiors that leapt to the forefront of home design in recent years is still popular, but homeowners can expect to see more bold colors in 2023. The kitchen island, cabinets, and backsplash are three target areas for adding color to your kitchen. These large surface areas are tailor-made for color splashes to lead the eye throughout the room. Experiment with complimentary tile designs, two-toned cabinets, and dark-stained wood to create a kitchen atmosphere that feels anything but bland.

In some ways, the design trends that defined 2022 will continue into next year. One such trend that will ring true in 2023 is a desire to fill the home with organic materials. Indoor plants will continue to be a popular decorative item throughout the home, both for their health benefits and their ability to mix and match with any décor style. In the living room, natural materials like stone, wood, and organic fabrics will help tie a home’s organic aesthetic together. And in the kitchen, stone and marble countertops add an earthy touch.

While bold colors are making their return to the kitchen, earth tones will help to balance out homeowners’ interior design palettes next year. Many design leaders’ color of the year selections for 2023 are in, all showcasing unconventional takes on earthy colors. Whether it’s beige, magenta, cream, or forest green, you can use these shades throughout your home to create balance and ground your bolder color choices elsewhere. Looking to swap out your grey couch? Have you always wanted to paint your gallery wall something other than off-white? Now is the time!

Homeowners have made significant adjustments to their lifestyles in recent years. For many, that’s meant spending time on their hobbies, exercising, and working on passion projects at home, whereas previously they may have gone elsewhere. After a couple years of making do with whatever space was available, moving forward, we’ll see a more intentional approach to creating space at home for those activities. Whether it’s building out a home gym, setting up your home office, craft room, art studio, yoga sanctuary, etc., having a dedicated area allows for privacy and focus while doing the things you love.

Image Source: Getty Images – Image Credit: Petar Chernaev

This past year, rising mortgage rates have slowed the red-hot housing market. Over the past nine months, we’ve seen fewer homes sold than the previous month as home price growth has slowed. All of this is due to the fact that the average 30-year fixed mortgage rate has doubled this year, severely limiting homebuying power for consumers. And, this month, the average rate for financing a home briefly rose over 7% before coming back down into the high 6% range. But we’re starting to see a hint of what mortgage interest rates could look like next year.

Inflation Is the Enemy of Long-Term Interest Rates

As long as inflation is high, we’ll see higher mortgage rates. Over the past couple of weeks, we’ve seen indications that inflation may be cooling, giving us a glimpse into what may happen in the future. The mortgage market is eagerly awaiting positive news on inflation. As Ali Wolf, Chief Economist at Zonda, says:

“The housing market is expected to face continued uncertainty heading into 2023 as consumers, financial markets, and policymakers work through their respective challenges in today’s economy. . . . we are watching for any additional stability in the MBS market, signs of cooling inflation, and/or less aggressive Federal Reserve action to give us confidence that mortgage rates are past their peak.”

What Does This Mean for the Future of Mortgage Rates?

As we get through the inflation battle and start to see that coming down, we should expect mortgage rates to follow. We’ve seen nods of this over the past couple of weeks. As the Federal Reserve works to bring inflation down, mortgage rates will come down as well. Bill McBride from Calculated Risksays:

“My current view is inflation will ease quicker than the Fed currently expects.”

As we look toward next year, we certainly hope he’s right.

Bottom Line

Mortgage rates will come down – it’s just a matter of time. The hope is we continue to see more positive news on inflation, and that’ll bring mortgage rates down. This will give prospective homebuyers more buying power and lead to more homeowners throughout the country.

While higher mortgage rates are creating affordability challenges for homebuyers this year, there is some good news for those people still looking to buy a home.

As the market has cooled this year, some of the intensity buyers faced during the peak frenzy of the pandemic has cooled too.

Here are just a few trends that may benefit you when you go to buy a home today.

1. More Homes To Choose from

During the pandemic, housing supply hit a record low at the same time buyer demand skyrocketed. This combination made it difficult to find a home because there just weren’t enough to meet buyer demand. According to Calculated Risk, the supply of homes for sale increased by 39.5% for the week ending October 28 compared to the same week last year.

Even though it’s still a sellers’ market and supply is still lower than more normal levels, you have more to choose from in your home search. That makes finding your dream home a bit less difficult.

2. Bidding Wars Have Eased

One of the top stories in real estate over the past two years was the intensity and frequency of bidding wars. But today, things are different. With more options, you’ll likely see less competition from other buyers looking for homes. According to the National Association of Realtors (NAR), the average number of offers on recently sold homes has declined. This September, the average was 2.5 offers per sale. In contrast, last September, the average was 3.7 offers per sale.

If you tried to buy a house over the past two years, you probably experienced the bidding war frenzy firsthand and may have been outbid on several homes along the way. Now you have a chance to jump back into the market and enjoy searching for a home with less competition.

3. More Negotiation Power

And when you have less competition, you also have more negotiating power as a buyer. Over the last two years, more buyers were willing to skip important steps in the homebuying process, like the appraisal or inspection, to try to win a bidding war. But the latest data from the National Association of Realtors (NAR) shows the percentage of buyers waiving those contingencies is going down.

As a buyer, this is good news. The appraisal and the inspection give you important information about the value and condition of the home you’re buying. And if something turns up in the inspection, you have more power today to renegotiate with the seller.

A survey from realtor.com confirms more sellers are accepting offers that include contingencies today. According to that report, 95% of sellers said buyers requested a home inspection, and 67% negotiated with buyers on repairs as a result of the inspection findings.

Bottom Line

While buyers still face challenges today, they’re not necessarily the same ones you may have been up against just a year or so ago. If you were outbid or had trouble finding a home in the past, now may be the moment you’ve been waiting for. Let’s connect to start the homebuying process today.

If you’re thinking about buying a home today, there’s welcome news. Even though it’s still a sellers’ market, it’s a more moderate sellers’ market than last year. And the days of feeling like you may need to waive contingencies or pay drastically over asking price to get your offer considered may be coming to a close.

Today, you should have less competition and more negotiating power as a buyer. That’s because the intensity of buyer demand and bidding wars is easing this year. So, if bidding wars were the biggest factor that had you sitting on the sidelines, here are two trends that may be just what you need to re-enter the market.

1. The Return of Contingencies

Over the last two years, more buyers were willing to skip important steps in the homebuying process, like the appraisal or inspection, to try to win a bidding war. But now, fewer people are waiving the inspection and appraisal.

The latest data from the National Association of Realtors (NAR) shows the percentage of buyers waiving their home inspection and appraisal is declining. And a recent survey from realtor.com confirms more sellers are accepting offers that include these conditions today. According to their August study:

95% of sellers reported buyers requested a home inspection

67% of sellers negotiated with buyers on repairs as a result of the inspection findings

This goes to show buyers are more able to include these conditions in their offers today and negotiate as needed based on the outcome of the inspection.

2. Sellers Are More Willing To Help with Closing Costs

Generally, closing costs range between 2% and 5% of the purchase price for the home. Before the pandemic, it was a common negotiation tactic for sellers to cover some of the buyer’s closing costs to sweeten the deal. This didn’t happen as much during the peak buyer frenzy over the past two years.

Today, as the market shifts and demand slows, data from realtor.com suggests this is making a comeback. A recent article shows 32% of sellers paid some or all of their buyer’s closing costs. This may be a negotiation tool you’ll see as you go to purchase a home. Just keep in mind, limits on closing cost credits are set by your lender and can vary by state and loan type. Work closely with your loan advisor to understand how much a seller can contribute to closing costs in your area.

Bottom Line

Regardless of the extremely competitive housing market of the past several years, today’s data suggests negotiations are starting to come back on the table. This is good news if you’re planning to enter the housing market. To find out how the market is shifting in our area, let’s connect.

If you’re following along with the news today, you’ve likely heard about rising inflation. You’re also likely feeling the impact in your day-to-day life as prices go up for gas, groceries, and more. These rising consumer costs can put a pinch on your wallet and make you re-evaluate any big purchases you have planned to ensure they’re still worthwhile.

If you’ve been thinking about purchasing a home this year, you’re probably wondering if you should continue down that path or if it makes more sense to wait. While the answer depends on your situation, here’s how homeownership can help you combat the rising costs that come with inflation.

Homeownership Offers Stability and Security

Investopediaexplains that during a period of high inflation, prices rise across the board. That’s true for things like food, entertainment, and other goods and services, even housing. Both rental prices and home prices are on the rise. So, as a buyer, how can you protect yourself from increasing costs? The answer lies in homeownership.

Buying a home allows you to stabilize what’s typically your biggest monthly expense: your housing cost. If you get a fixed-rate mortgage on your home, you lock in your monthly payment for the duration of your loan, often 15 to 30 years. James Royal, Senior Wealth Management Reporter at Bankrate, says:

“A fixed-rate mortgage allows you to maintain the biggest portion of housing expenses at the same payment. Sure, property taxes will rise and other expenses may creep up, but your monthly housing payment remains the same.”

So even if other prices rise, your housing payment will be a reliable amount that can help keep your budget in check. If you rent, you don’t have that same benefit, and you won’t be protected from rising housing costs.

Use Home Price Appreciation to Your Benefit

While it’s true rising mortgage rates and home prices mean buying a house today costs more than it did a year ago, you still have an opportunity to set yourself up for a long-term win. Buying now lets you lock in at today’s rates and prices before both climb higher.

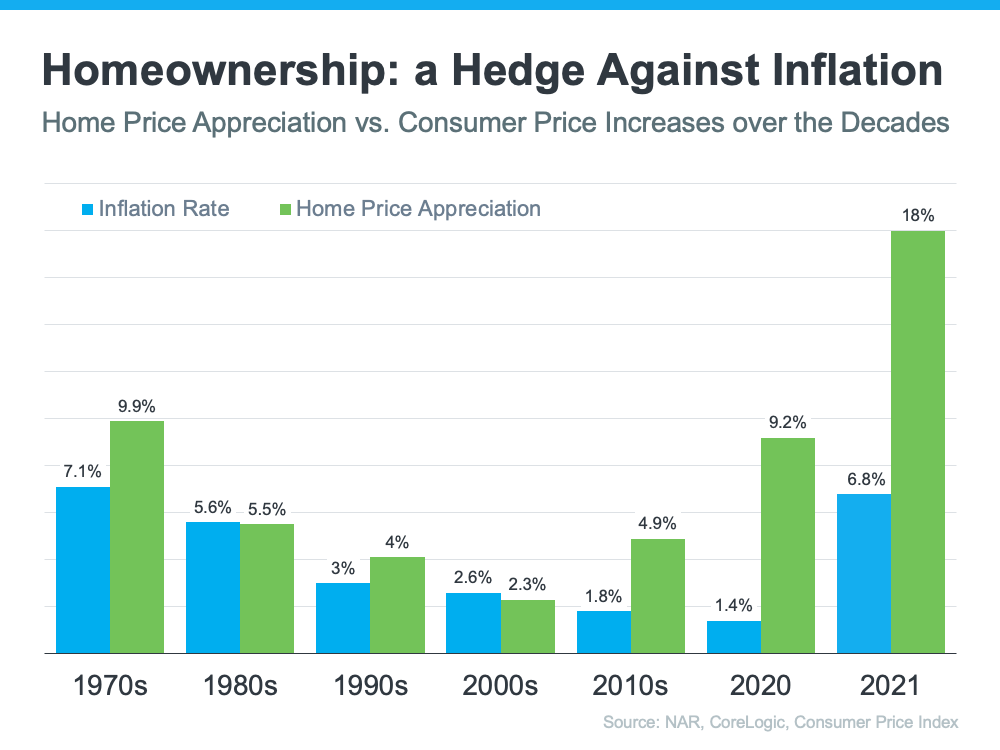

In inflationary times, it’s especially important to invest your money in an asset that traditionally holds or grows in value. The graph below shows how home price appreciation outperformed inflation in most decades going all the way back to the seventies – making homeownership a historically strong hedge against inflation (see graph below):

So, what does that mean for you? Today, experts say home prices will only go up from here thanks to the ongoing imbalance in supply and demand. Once you buy a house, any home price appreciation that does occur will be good for your equity and your net worth. And since homes are typically assets that grow in value (even in inflationary times), you have peace of mind that history shows your investment is a strong one.

Bottom Line

If you’re ready to buy a home, it may make sense to move forward with your plans despite rising inflation. If you want expert advice on your specific situation and how to time your purchase, let’s connect.

In a recent research paper, Homeownership and the American Dream, Laurie S. Goodman and Christopher Mayer of the Urban Land Institute explained:

“Homeownership appears to help borrowers accumulate housing and non-housing wealth in a variety of ways, with tax advantages, greater financial flexibility due to secured borrowing, built-in ‘default’ savings with mortgage amortization and nominally fixed payments, and the potential to lower home maintenance costs through sweat equity.”

Let’s breakdown 5 major financial benefits of homeownership:

1. Housing is typically the one leveraged investment available

Homeownership allows households to amplify any appreciation on the value of their homes by a leverage factor. A 20% down payment results in a leverage factor of five, meaning every percentage point rise in the value of your home is a 5% return on your equity. If you put down 10%, your leverage factor is 10.

Example: Let’s assume you purchased a $300,000 home and put down $60,000 (20%). If the house appreciates by $30,000, that is only a 10% increase in value but a 50% increase in equity.

2. You’re paying for housing whether you own or rent

Some argue that renting eliminates the cost of property taxes and home repairs. Every potential renter must realize that all the expenses the landlord incurs (property taxes, repairs, insurance, etc.) are baked into the rent payment already – along with a profit margin!!

3. Owning is usually a form of “forced savings”

Studies have shown that homeowners have a net worth that is 44X greater than that of a renter. As a matter of fact, it was recently estimated that a family buying an average priced home this past January could build more than $42,000 in family wealth over the next five years.

4. Owning is a hedge against inflation

House values and rents tend to go up at or higher than the rate of inflation. When you own, your home’s value will protect you from that inflation.

5. There are still substantial tax benefits to owning

We know that the new tax reform bill puts limits on some deductions on certain homes. However, in the research paper referenced above, the authors explain:

“…the mortgage interest deduction is not the main source of these gains; even if it were removed, homeowners would continue to benefit from a lack of taxation of imputed rent and capital gains.”

Bottom Line

From a financial standpoint, owning a home has always been and will always be better than renting.

According to a new study from Urban Institute, there are over 19 million millennials in 31 cities who are not only ready and willing to become homeowners, but are able to as well!

Now that the largest generation since baby boomers has aged into prime homebuying age, there will no doubt be an uptick in the national homeownership rate. The study from Urban Institute revealed that nearly a quarter of this generation has the credit and income needed to purchase a home.

Surprisingly, the largest share of mortgage-ready millennials lives in expensive coastal cities. These cities often attract highly skilled workers who demand higher salaries for their expertise.

So, what’s holding these mortgage-ready millennials back from buying?

Myths About Down Payment Requirements!

Most of the millennials surveyed for the study believe that they need at least a 15% down payment in order to buy a home when, in reality, the median down payment in the US in 2017 was just 5%, and many programs are available for even lower down payments!

The study goes on to point out that:

“Despite limited awareness, every state has programs that provide grants and loans to make homeownership more attainable, with average assistance in various states ranging from $2,436 to $21,171.”

Bottom Line

With so many young families now able to buy a home in today’s market, the demand for housing will continue for years to come. If you are one of the many millennials who have questions about their ability to buy in today’s market, let’s get together so we can assist you along your journey!

Are you stuck in the San Diego renter’s trap? Is it time for you to consider buying? Let’s explore that question and talk about points to consider along with steps to take that will ensure longterm comfort.

Here’s the scenario…you are living and leasing in San Diego County and you’re frustrated with rising rents as well as lack of longterm housing stability. The idea of what you may be paying for rent five years from now is a daunting thought. You’ve considered purchasing a home for one or more of the following reasons:

To secure a consistent monthly housing payment for the next 30 years, unlike renting

For the peace of mind that you have a roof, YOUR roof, over your head. Your landlord can’t increase your rent or sell the place your living in and leave you searching for another home

If you wait you could be priced out and may never be able to own a home of your own in San Diego

Your buying power will decrease over time with rising interests rates

As an investment…to build real equity overtime that can someday be handed off to your children

All of these are valid reasons to consider. In fact, these are the thoughts that have been going through my mind for the last year or two. So this blog piece is quite personal. Tackling the question “to buy or not to buy” has become a research obsession of mine. You’re not alone. So let’s dive in together and figure this out.

Let’s Talk About Buying Power

At the forefront of these concerns are interest rates. Although rising, we are still seeing historically low rates. Rates are expected to rise over the next 2-3 years and are forecasted by Windermere’s Chief Economist, Matthew Gardner, to increase 2.9% by 2020 (this number is very in sync with most economists and housing market specialists).

For every 1% increase in interest rates, your buying power goes down 10%. That means if today you can afford a home that is 600k, in two to three years just the increase in interest rates will decrease your buying power by $60,000… in addition to your monthly payment increasing.

To Buy or Not to Buy? That is the Question.

But, Kara, what if I buy now and it ends up being at the peak of the market? Maybe I should wait until the market crashes and I can buy at the bottom. These are valid questions and concerns. I don’t have a crystal ball…sure wish I did for all of us…myself included. I am constantly researching and listening to all economists out there and looking at key predictors.

Here’s what I’ve heard and seen:

Home values in SD will continue to rise at a more sustainable rate…very unlike the double digit increases we have seen in some areas over the last couple of years

99% of Real Estate analysts predict homes will continue to appreciate, especially in markets like San Diego County

Interest rates will go up (2% in the next few years as discussed above)

The rental market will become more competitive and expensive (it will, if not already, absorb 40% of your income)

And yes, we will have a recession. It is inevitable. Every 10 or so years it happens. However, it will NOT be what it was in 2007 for many reasons, including, stricter lending policies. It will look more like the 1990 recession…very shallow and skinny

This Gets Personal

In this market it’s all about your personal situation and intent. Below are a few points to consider.

If your intention is to hang onto the home you purchase indefinitely, or let’s say at least seven years, buy now. If you are financing most of the purchase with a mo

rtgage, this will allow you to take advantage of lower interest rates before they rise, thus keeping your longterm monthly payments low and your buying power high. When considering renting longterm vs. buying to hold longterm, future home price changes are less important than your fixed monthly mortgage payment. Imagine what you might be paying in rent 10 years from now!

Home prices may decline at some point, but they may not. Either way, you will have locked in a reasonable monthly payment for the long haul, and this is likely more important than changes in the market price of a house you have no intent to sell any time soon.

However, if you are not sure how long you will live in this area and may have to sell in the next couple of years, that’s another story. This may result in low potential gains as you may be selling at a loss IF home prices do decline. The benefits of low monthly payments in the short term do not outweigh the risk of the potential loss. Potential shorter-term buyers should proceed with caution.

Why Not Explore Your Options?

So, all that being said, your plan is to buy and hold or at least look into what it would look like financially to do so. What’s the first step? Connect with a loan officer. I have two preferred lenders I can connect you with that are no pressure, with accurate and detailed information.

Find out what it would take to buy in the next 3- 6 months, explore what you would be qualified for and what that monthly mortgage payment would look like. If you don’t think you’re ready to buy that soon, still chat with them and myself. There are things we can do to get your ducks in a row…from reviewing your credit to setting you up on my MLS linked website so you can become educated on the market in neighborhoods you are interested in.

Hurdles and Roadblocks

Don’t think you have enough down payment? Long are the days that it takes 20% down to purchase a home. There are loans available for as little as 3% down and if you’re a veteran it’s even lower. Credit not so good? FHA loans allow those interested in purchasing to do just that with a mortgage that’s insured by the Federal Housing Administration (FHA). There are options out there and it doesn’t take long to get answers from Dan.

Or perhaps you chat with Dan and he brings to your attention that you have some credit issues (oh my!) to deal with. You may already be aware and are hoping those negative marks would just miraculously disappear? Really, truly you are not alone.

But by all means, don’t wait! Get right on it and work with someone that can quickly (and affordably) remedy these credit thorns in your side. Bad credit can cost you when financing a home so first step is to get it as clean and clear as possible. My clients use Nicole Soares with bSquared Credit and are thrilled with the results. She and her team offer a free consultation… so there you have it…no more excuses.

Seek Comfort and Longterm Stability

Now here’s a point that I always drive home with my clients…make sure you are comfortable with the total monthly payment. Often times we get excited to be approved at say, 700k, but perhaps the monthly payment is really NOT that realistic for you financially. I don’t ever want my clients to be house poor and stressed.

Work with your lender and calculate the monthly payment once you know what you are qualified for (taking everything into consideration…taxes, HOA fees, private mortgage insurance if you are not putting 20% down or if you have an FHA loan). Or even better, if you know what the max monthly payment is that you are comfortable with, start there with a lender. Work backwards. Let the monthly payment drive your maximum purchase price.

Here is a great monthly mortgage payment website with calculators that result in a REAL number. (Reach out to me or your lender if you have questions.) My goal is to get my clients into a home at a price that they are comfortable, content and happy with over many, many years. Not the one that is the most expensive that results in the highest commission.

The Search is ON

Once you identify a maximum purchase price and a monthly mortgage you are comfortable with, I can then take the qualifying numbers and start sending you properties that fit your parameters and maximum purchase amount. It is time to check out properties and find your new home. This is the fun part! It can take awhile to find the right place. I am patient and there for you every step of the way. I will do everything in my power to make purchasing a home as enjoyable and stress-free as possible.

Let’s work together to find out if now is the right time for you to buy and if so, what does that realistically look like for you. Every situation is different and I am here to help.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link