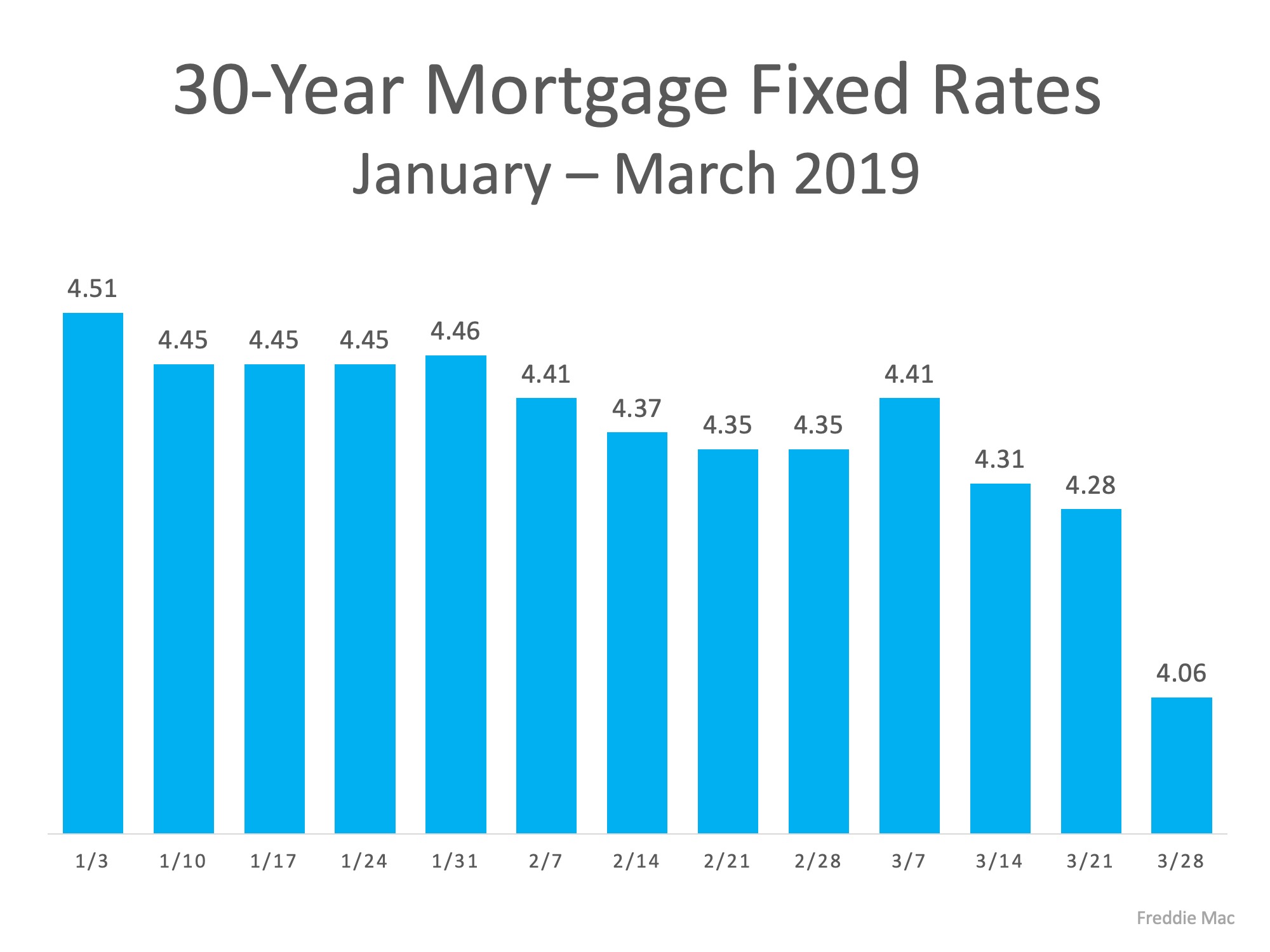

Interest rates for a 30-year fixed rate mortgage have been on the decline since November, now reaching lows last seen in January 2018. According to Freddie Mac’s latest Primary Mortgage Market Survey, rates came in at 4.12% last week!

This is great news for anyone who is planning on buying a home this spring! Freddie Mac had this to say,

“Mortgage interest rates have been steadily declining since the start of 2019. These lower mortgage interest rates combined with a strong labor market should attract prospective homebuyers this spring and could help the housing sector regain its momentum later in the year.”

To put the low rates in perspective, the average for 2018 was 4.6%! The chart below shows the recent drop, and also shows where the experts at Freddie Mac believe rates will be by the end of 2019.

Bottom Line

If you plan on buying a home this year, let’s get together to start your home search to ensure you can lock in these historically low rates today!

The Housing Market has been a hot-topic in the news lately. Depending on which media outlet you watch, it can start to be a bit confusing to understand what’s really going on with interest rates and home prices!

The best way to show what’s really going on in today’s real estate market is to go straight to the data! We put together the following three graphs along with a quote from Chief Economists that have their finger on the pulse of what each graph illustrates.

Interest Rates:

“The real estate market is thawing in response to the sustained decline in mortgage rates and rebound in consumer confidence – two of the most important drivers of home sales. Rising sales demand coupled with more inventory than previous spring seasons suggests that the housing market is in the early stages of regaining momentum.” – Sam Khater, Chief Economist at Freddie Mac

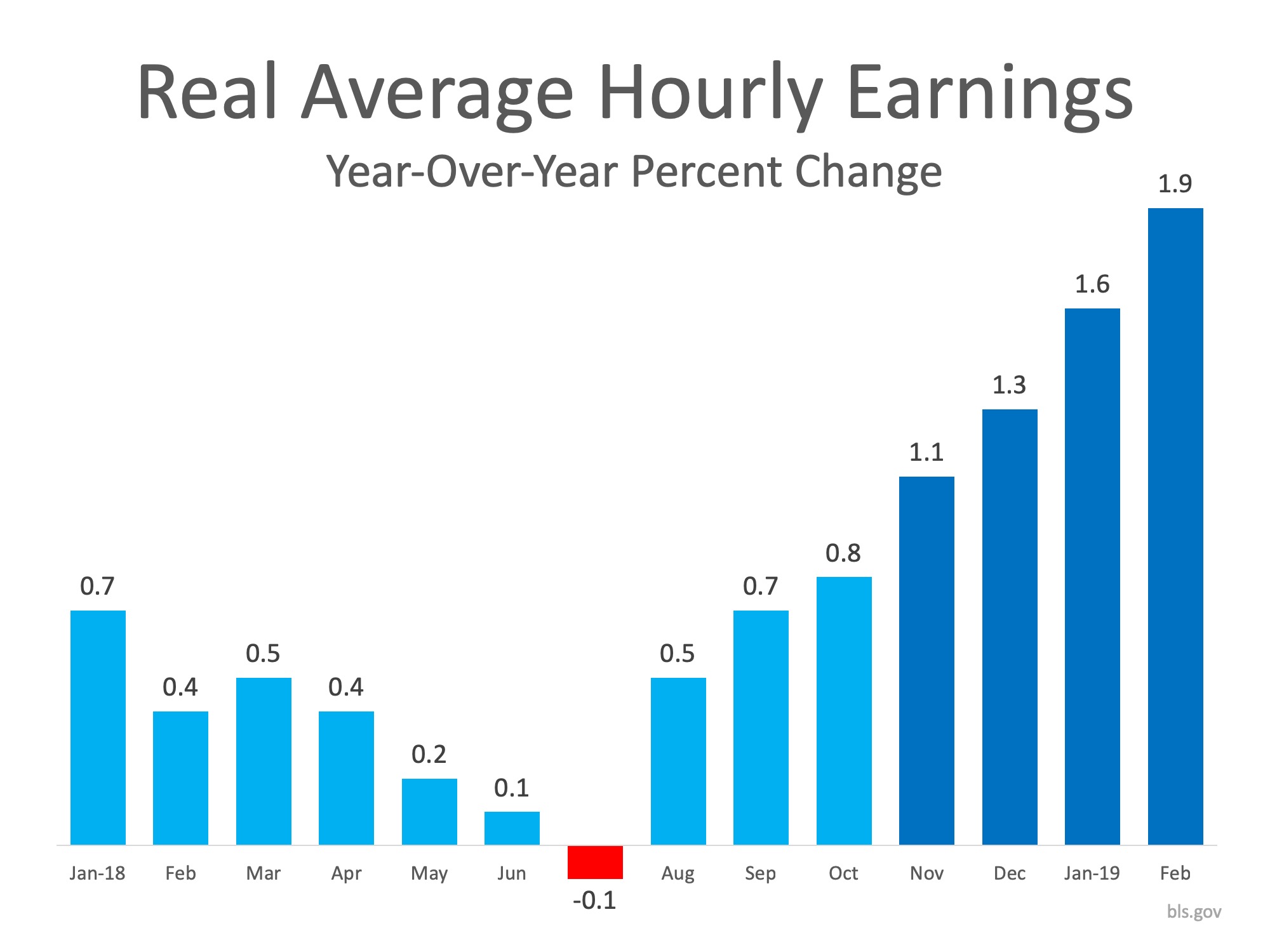

Income:

“A powerful combination of lower mortgage rates, more inventory, rising income and higher consumer confidence is driving the sales rebound.” – Lawrence Yun, Chief Economist at NAR

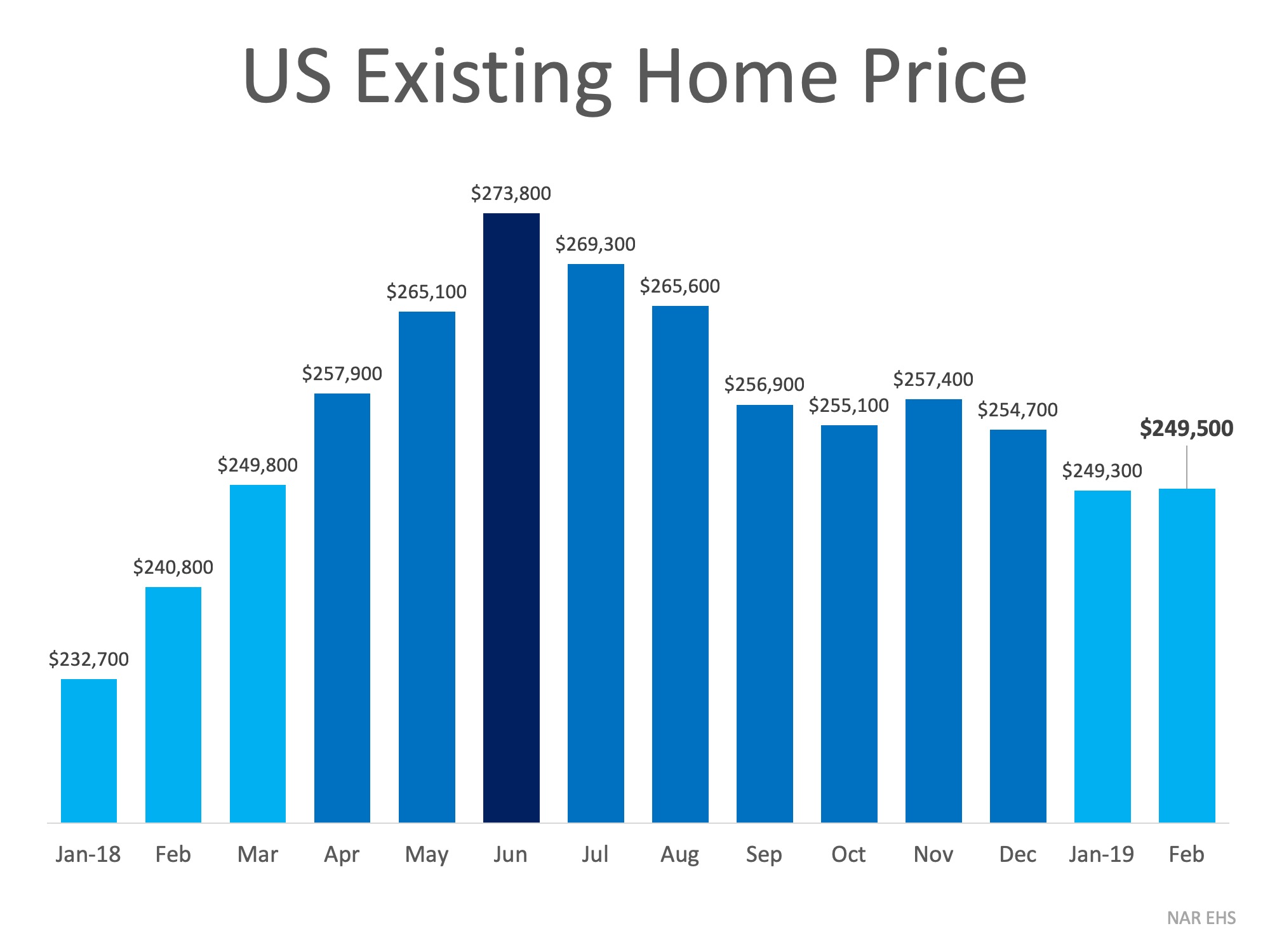

Home Prices:

“Price growth has been too strong for several years, fueled in part by abnormally low interest rates. A mild deceleration in home sales and Home PriceIndex growth is actually healthy, because it will calm excessive price growth — which has pushed many markets, particularly in the West, into overvalued territory.” – Ralph DeFranco, Global Chief Economist at Arch Capital Services Inc.

Bottom Line

These three graphs indicate good news for the spring housing market! Interest rates are low, income is rising, and home prices have experienced mild deceleration over the last 9 months. If you are considering buying a home or selling your house, let’s get together to chat about our market!

Are you and your partner ready to cohabitate? Making that decision is often exciting and nerve-wracking at the same time. Thankfully, keeping a few dollar-stretching strategies in mind means outfitting your new place can add to the fun without adding to your stress.

Out with the old

Every household has basics, so most couples discover they have several duplicate items when they move in together. Take some time to sort through what you both have, decide what you need to acquire, and think about what items are due for an upgrade. Pay special attention to tablecloths, gadgetry, cookware, and the like. NBC News points out kitchen items in particular need routine replacement, with non-stick cookware warranting extra consideration, since worn or peeling cookware should be thrown out and replaced. Make some notes to ensure you have all your basics covered, and develop a shopping list for the items you need or want to purchase together. You can buy everything from new linens to small appliances from retailers like Kohl’s, and on top of a great selection, Kohl’s promo codes help you make the most of your budget.

Color your world

With your essentials in order, addressing aesthetics is a logical next step. Many couples add a fresh coat of paint to their new digs to give it their personal touch, so sit down together and discuss what shades in which rooms sound appealing. Elle Decor points out many of the hottest color trends incorporate hues from the great outdoors, such as shades borrowed from woodlands in earthy browns, rich greens, and deep blues. If you never painted before or haven’t done so as a joint project, brush up on basic how-to instructions, gather your supplies, and do your shopping someplace like Ace Hardware, where you can find everything you need for your project as well as take advantage of great deals.

Bedroom basics

Refreshing your bedroom can help you get started on the right foot. Beyond the walls, consider revamping the color scheme in hues you both like, whether it’s soothing tones of teal and tan, cheerful coral and fuschia, or bold black and red. Think accents, sheets, and even furniture colors. And while you’re at it, consider investing in a new mattress and foundation. It’s the perfect symbol of your decision to share space. Some experts recommend replacing mattresses every seven to 10 years anyway, so if yours falls into that age range, all the more reason to start anew. Then select appropriate linens to fit your new bed and colors. You can shop online for the whole shebang from stores like Overstock, offering everything you need to dress your bedroom in style, just check out their current sales to ensure you snag great prices.

Sharing storage

Divvying up your closet space can seem simple at first, but many couples quickly discover making room for two sets of clothes can be a challenge. There are plenty of ways you can improve the storage you have by adding drawers and shelving, or you can install a closet system. If you or your partner is pretty handy, Family Handyman points out you can install a DIY closet system in a weekend, which can be a fun project to take on together. Home Depot offers a wide variety of closet organization solutions, which you can DIY or have installed for you. Take some measurements, make some sketches, and check Home Depot’s current offers to see what will work well in your space as well as your budget.

Combining your lives can be challenging, so make sure putting your home together isn’t a major financial stressor. Look for smart and economical ways to outfit your home, make decisions together, and add some new things to signify your change. When you’re taking that next step, it’s a great way to keep things light, positive, and fun.

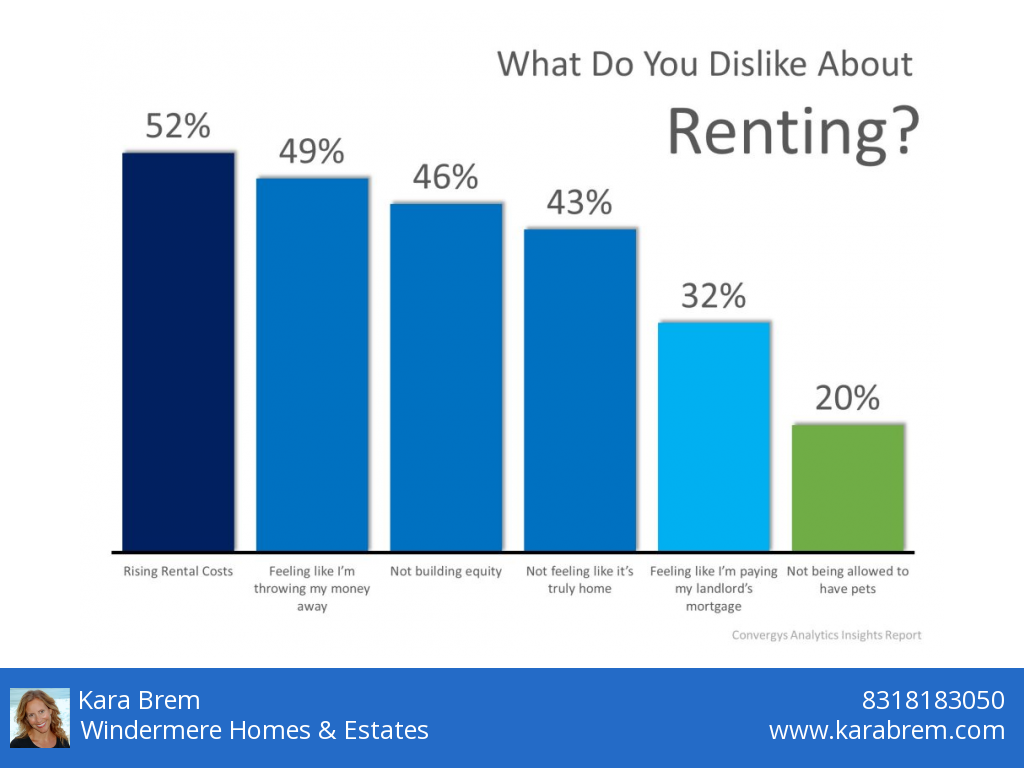

The largest obstacle renters face when planning to buy a home is saving for a down payment. This challenge is amplified by rising rents, which has eaten into the amount of money renters have leftover for savings each month after paying expenses.

In combination with higher rents, survey after survey has shown that non-homeowners (renters and those living rent-free with family or friends) believe they need to save upwards of 20% for their down payment!

According to the “Barriers to Accessing Homeownership” study commissioned in partnership between the Urban Institute, Down Payment Resource, and Freddie Mac,39% of non-homeowners and 30% of those who already own a home believe they need more than a 20% down payment.

The percentage of those who are aware of low down payment programs (those under 5%) is surprisingly low at 12% for non-homeowners and 13% for homeowners.

In a recent Convergys Analytics report, they found that 49% of renters believe they need at least a 20% down payment.

The median down payment on loans approved in 2018 was only 5%! Those waiting until they have over 20% may already have enough saved to buy now!

There are over 45 million millennials (33%) who are mortgage ready right now, meaning their income, debt, and credit scores would all allow them to qualify for a mortgage today!

Bottom Line

If your five-year plan includes buying a home, let’s get together to determine what it will take to make that plan a reality. You may be closer to your dream than you realize!

For many seniors, there comes a time when the expense and upkeep of a big home no longer seem realistic. All of your kids have moved out, and suddenly, your multi-bedroom house feels excessively large and empty. Plus, it may be difficult to keep up with mortgage payments if you’re expecting a lower income during retirement. Whether downsizing is a financial necessity or an emotional decision, here’s how to tackle the process without getting overwhelmed.

Do Online Research

Before you start looking at houses in person, narrow down your options by doing some research online. Search the local housing market on sites or reach out to a Realtor to get a feel for house prices in your desired area. Explore listings in your preferred size range and location so you can come up with a realistic budget for your new home.

Think far ahead as you look at homes, considering the possibility that the needs of you and your spouse may change over time. One-story homes can be much more accessible for you and your friends down the line. You should also take time to research the neighborhood and pay attention to the house’s proximity to grocery stores, leisure centers, and public transportation.

Plan for Your Storage Needs

If you’re moving to an apartment or condo, you may not have the attic, basement, or even the closet space that you’re used to. Look for a nearby for an affordable self-storage unit so you aren’t left crowding boxes and furniture into your new home. Some simple online research can help you find the best deals in your area.

Go Through Your Possessions Methodically

One of the hardest parts about downsizing is getting rid of things you’ve had for decades. Apartment Guide recommends looking at pictures of clutter-free homes in magazines or do a search on google for inspiration before starting your own purge. This will mentally prepare you for getting rid of all the stuff you don’t need cluttering up your new, smaller space.

As you declutter, go room by room and sort items into no more than five piles: keep, donate, sell, gift, and throw away. Don’t be afraid to let go of things that are useful but not particularly necessary in your own life. Likewise, don’t keep things out of obligation or feelings of guilt. While you’re cutting the clutter, keep a floor plan of your new home nearby so you can plan out your rooms and ensure your furniture will fit.

Pack Like a Pro

Protect your items during your move and make them easier to unpack later by trying out some expert packing tips. For example, socks make great padding for glasses and mugs, while oven mitts are perfect for transporting knives a little more safely. Secure entire desk drawers and kitchen storage trays with plastic wrap for much faster unpacking later. Also, keep your clothing on hangers and simply slip a garbage bag over them for protection. Remember to pack an essentials box of everything you need during your first day and night in your new house.

Follow a Moving Checklist

There is a lot to remember to do before moving day. For example, you need to update your mailing address with the post office, find a new doctor, and transfer your utilities. Follow a moving checklist (or hire a senior move manager for around $316 per day) to avoid forgetting important tasks. One of your moving tasks should involve researching moving companies at least two months before your move. This gives you plenty of time to find the help you need within your budget. Learn about how to spot rogue moving companies so you can avoid being scammed, especially if you’re moving long distance.

Moving is exhausting for anyone. But moving into a smaller home can be especially emotional as you say goodbye to personal objects that have surrounded you for much of your life. For this reason, it’s important to take things slow while you sort through your possessions and search for the perfect place to spend your golden years.

Downsizing is both freeing and stressful. It’s never easy to pare down a lifetime of memories, and most of us tend to associate our belongings with events and the people we love. Here are some downsizing tips to help make sure you don’t make any mistakes, but pare down enough to happily move to a smaller home or apartment.

Browse beautiful rooms & contemplate simplicity

You can simply thumb through magazines and books, or peruse the beautiful images of Houzz.com. Pay attention to how little clutter you see. Pay attention to the positive feelings you have about those simplified rooms. Get yourself mentally prepared – if not excited – that you have the opportunity to live in a simpler space, a space filled with ONLY the things you love.

Hot Tip: Tape a photo of a beautiful, simplified room into each room of your home; they can inspire you during your purge.

Think, too, about how many things you own that you haven’t actually used, touched or even seen in over a year. Focus on the joy you will feel by donating, selling or giving those items away. No matter which option you choose, you win.

Ask who wants some of your belongings

Ask family members and close friends if they would be interested in any of your belongings before you start to sort. Ask them to list what type of items they might be interested in, or to make any specific requests (in case someone loves a particular painting, memento or piece of furniture). If you don’t get a reply – especially from those under the age of about 30 – make a mental note to save a few things for them ANYWAY. They might be too young to know the value of sentiment.

Buy Rubber Tubs for Items You’ll be Gifting

These are your gift tubs; we recommend rubber tubs with lids that seal tight. Think of them like a lovely gift, because they are. With each piece of jewelry, photo, letter, memento, homemade quilt or old letter jacket, you are filling this box with treasures that are sure to elicit a smile. Picture future generations of your family enjoying or telling stories about these items. Label your tubs and put them in one room of the house.

If you have lots of family pics, consider one gallery wall of favorites. Ask your children to take or digitize the remaining images.

Identify items you absolutely LOVE or CHERISH

Picture having to quickly evacuate your home. What few items would utterly devastate you if they were lost? (We’re not talking about collectibles with value; we’ll get to those in a minute). These are likely photos, letters, artwork, handmade gifts or things you made, jewelry, a small family heirloom, perhaps an item or two from your travels. What sentimental items would you save from a burning house? Gather or identify these items first (sticky notes might help, or start a list).

Keep this selection deliberately small. It’s special. There’s another level of belongings you can keep which are non-critical. But a ‘personal treasure’ pile should fit in your backseat.

Room by Room: Gift, Sell, Donate or Trash

Now you’re ready to go room by room and learn the extraordinary feeling of lightness that a purge can bring. There are the four categories that matter most to you now: gift, sell, donate, trash. The more items you can identify for each category, the happier you will be (and the lighter your load at moving time). Tackle your home room by room; you’ll have a larger feeling of accomplishment that way.

If you have the space to do so, move items you plan to sell or donate into dedicated spaces, like the garage or a spare room. Fill your rubber gift tubs. And think about how you’d like to sell other items. There’s ebay (yourself or through a hired seller); consignment stores; online apps and Facebook sale pages; a garage sale; or – if you amass enough items – an estate sale or auction. It won’t be long before you get a rush from filling your trash cans. You can do it!

It also helps to have a floor plan of your new home, with the dimensions on it. Measure your favorite furnishings and figure out which pieces will comfortably fit into new spaces, and which should find a new home. There’s fun in acquiring a few pieces for a smaller home, and selling, auctioning or consigning older furnishings and collectibles might well cover those expenses.

Hot Tip: Many cities have thrift stores and organizations which will pick up items if scheduled on the day the truck goes to your neighborhood.

Don’t throw out a high school letter jacket or other special personal items without giving your children a chance to claim them.

Where to be careful

There are a few mistakes you can make. One is getting rid of your children’s items without telling them. Give adult children a deadline by which to claim their left-behind items. Send them pics from your phone if they’re far away. Offer to ship them a box but don’t consider moving their items to your smaller home. The time has come. You are no longer obligated to store their old school yearbooks or letter jackets, cheerleading uniforms or trophies.

If you’re downsizing after a tragedy, don’t go overboard. You might consider putting some things in storage for a year, or having a friend help you decide what to keep. Emotions run high after unexpected events, and if you’re depressed, you may get rid of things you’ll want later. Don’t, however, use this as an excuse to keep everything.

The last warning: don’t be sloppy when it comes to collectibles. Set them aside until you can get them evaluated by an expert, or at least a friend or relative with a computer. These might include baseball cards, signed memorabilia, vintage toys or artisan crafted pieces.

Items you only need ONE of

Here’s a quick list to help you pare down some things of which we all accumulate extras. these are items you likely only need one of

Set of dishes

Set of glassware

Set of tupperware

Set of mixing bowls

Large serving platter

Household tools (hammer, screwdriver, tape measure)

Extra blankets (keep one heavy and one light, per guest bed)

Large winter and summer purse

Coat for each type of weather (extra warm, lighter weight, rain jacket, windbreaker)

Umbrella (one travel size, one oversized)

Cooler (you might keep a small one for car trips or picnics with grandkids)

Set of small tools, measuring tape

Hot Tip: Remember that donations will be a tax write-off. Always get a receipt.

Items you won’t need in an apartment or smaller home

Ladders larger than a step-stool

Garden tools

Wheelbarrow

Large power tools

Excessive outdoor Christmas decorations

Hot Tip: If an item’s been in a box for more than a year, it’s very likely time to let it go.

[find-an-apartment]

Ask a friend or professional to help

If you have trouble with decision-making, ask someone impartial to help you, someone who embraces your goal. A friend won’t have the same emotional attachment to your items, and can help you narrow down your belongings, while ALSO helping make sure you keep what you love. A professional or aspiring home organizer is a great investment. They will be efficient while also being kind.

As we kick off the new year, many families have made resolutions to enter the housing market in 2019. Whether you are thinking of finally ditching your landlord and buying your first home or selling your starter house to move into your forever home, there are two pieces of the real estate puzzle you need to watch carefully: interest rates & inventory.

Interest Rates

Mortgage interest rates had been on the rise for much of 2018, but they made a welcome reversal at the end of the year. According to Freddie Mac’s latest Primary Mortgage Market Survey, rates climbed to 4.94% in November before falling to 4.62% for a 30-year fixed rate mortgage last week. Despite the recent drop, interest rates are projected to reach 5% in 2019.

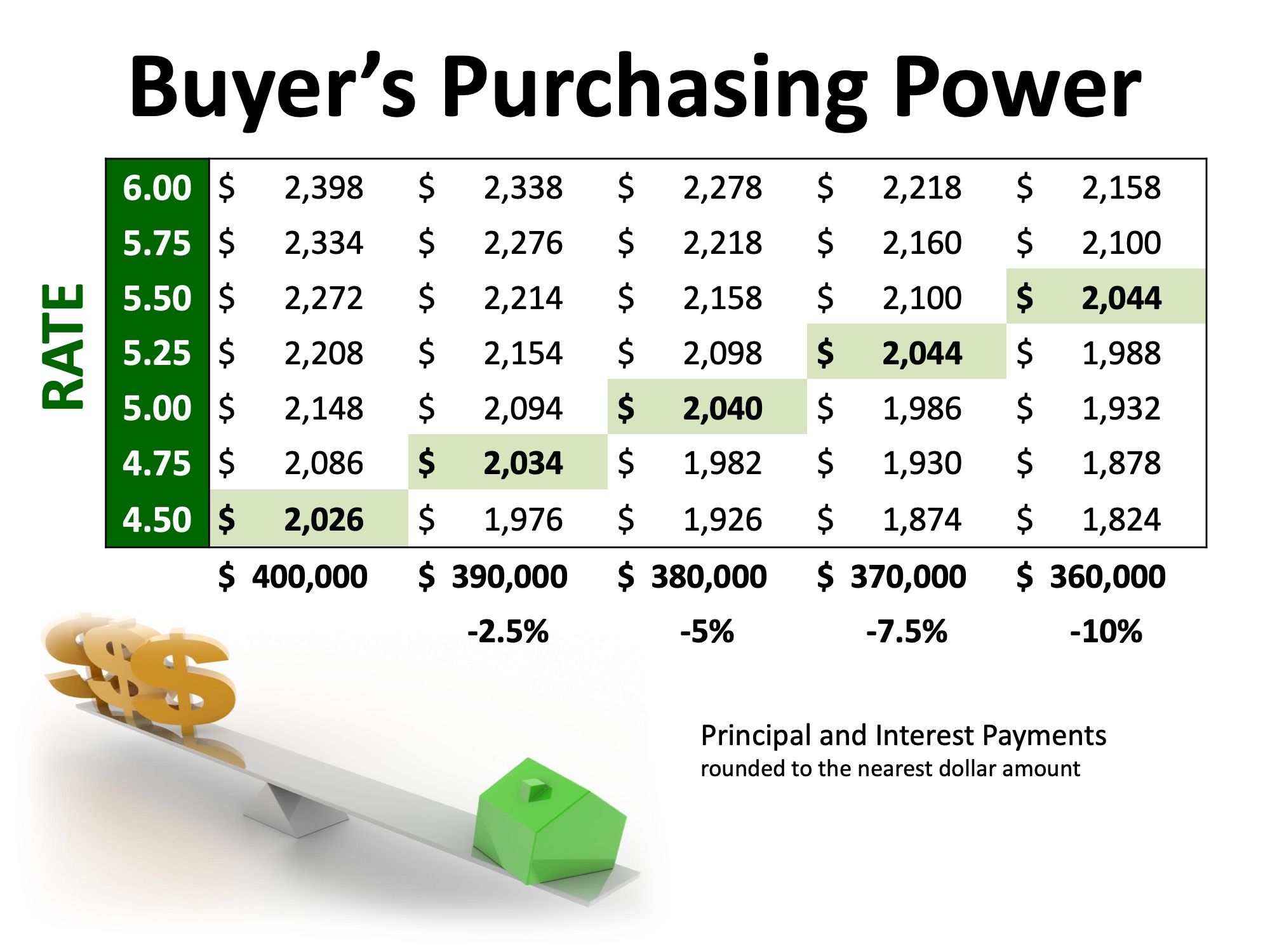

The interest rate you secure when buying a home not only greatly impacts your monthly housing costs, but also impacts your purchasing power.

Purchasing power, simply put, is the amount of home you can afford to buy for the budget you have available to spend. As rates increase, the price of the house you can afford to buy will decrease if you plan to stay within a certain monthly housing budget.

The chart below shows the impact that rising interest rates would have if you planned to purchase a $400,000 home while keeping your principal and interest payments between $2,020-$2,050 a month.

With each quarter of a percent increase in interest rate, the value of the home you can afford decreases by 2.5% (in this example, $10,000).

Inventory

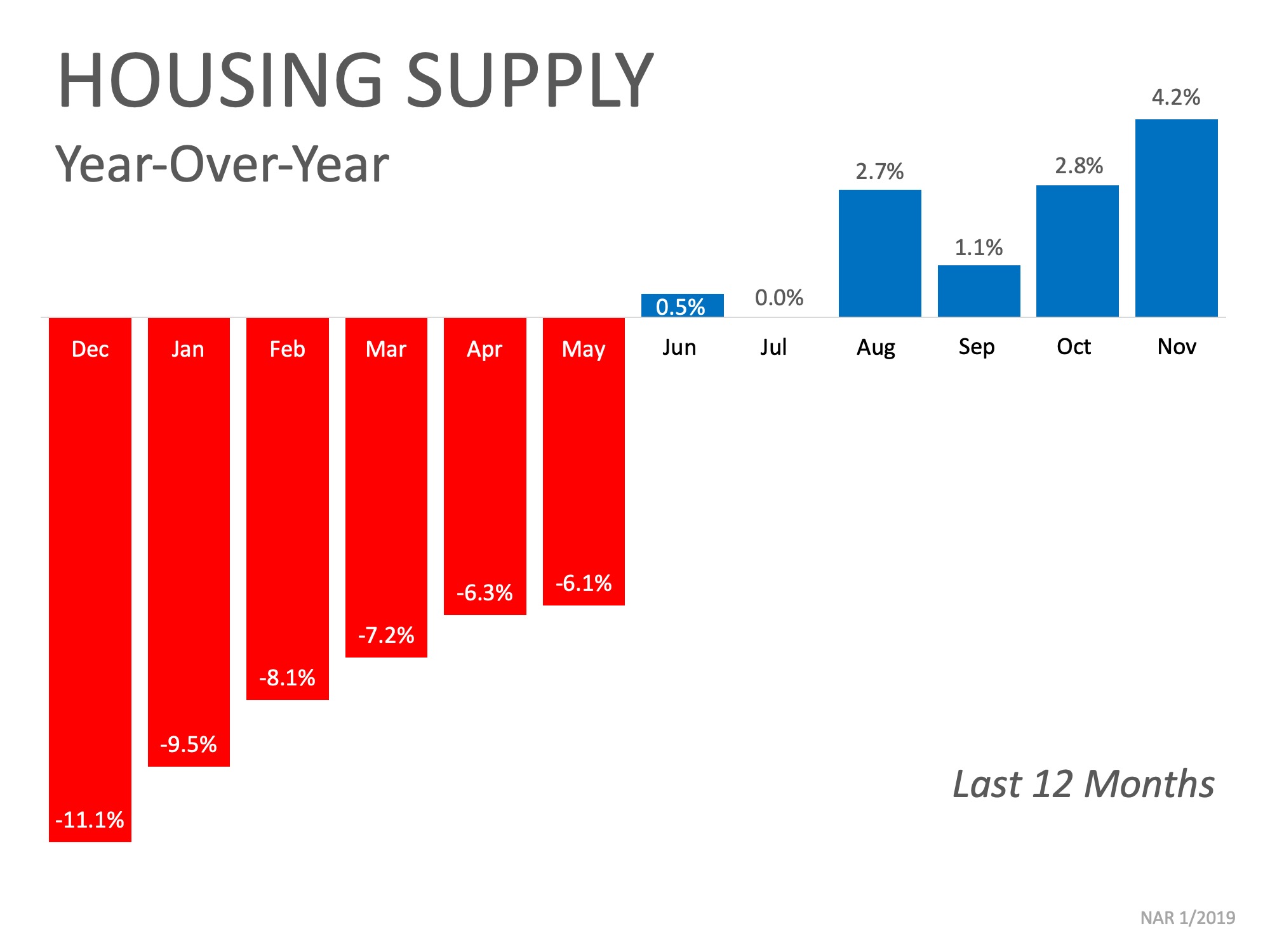

A ‘normal’ real estate market requires there to be a 6-month supply of homes for sale in order for prices to increase only with inflation. According to the National Association of Realtors (NAR), listing inventory is currently at a 3.9-month supply (still well below the 6-months needed), which has put upward pressure on home prices. Home prices have increased year-over-year for the last 81 straight months.

The inventory of homes for sale in the real estate market had been on a steady decline and experienced year-over-year drops for 36 straight months (from July 2015 to May 2018), but we are starting to see a shift in inventory over the last six months.

The chart below shows the change in housing supply over the last 12 months compared to the previous 12 months. As you can see, since June, inventory levels have started to increase as compared to the same time last year.

This is a trend to watch as we move further into the new year. If we continue to see an increase in homes for sale, we could start moving further away from a seller’s market and closer to a normal market.

Bottom Line

If you are planning to enter the housing market, either as a buyer or a seller, let’s get together to discuss the changes in mortgage interest rates and inventory and what they could mean for you.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

![Slaying the Largest Homebuying Myths Today [INFOGRAPHIC] | MyKCM](https://karabrem.com/files/2019/04/Slaying-Myths-ENG-MEM.jpg)

![Slaying the Largest Homebuying Myths Today [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2019/04/03102557/Slaying-Myths-ENG-MEM-1046x1477.jpg)