Today’s mortgage rates and home prices may have you second-guessing whether it’s still a good idea to buy a home right now. While market factors are definitely important, there’s also a bigger picture to consider: the long-term benefits of homeownership.

Think of it this way. If you know people who bought a home 5, 10, or even 30 years ago, you’re probably going to have a hard time finding someone who regrets their decision. That’s because over time, home values usually grow – and that means a homeowner’s net worth does too. Here’s a look at how that can really add up over the years.

Home Price Growth over Time

The map below uses data from the Federal Housing Finance Agency (FHFA) to show how much prices have grown over the last five years. Since home prices vary by area, the map is broken out regionally to really showcase larger market trends:

You can see that nationally, home prices increased by over 57% in just five years.

Some regions are slightly above or below that average, but overall, home prices saw a big uptick in a short time. And if you zoom out even more, the benefit of homeownership — and the drastic gains homeowners made over the years — become even more clear (see map below):

The second map shows that, over a roughly 30-year span, home prices appreciated by an average of more than 320% nationally.

So the typical homeowner who bought a house about 30 years ago saw their home triple in value during that time. And that’s a major reason so many homeowners who bought their homes years ago are still happy with their decision today.

Bottom Line

There’s no denying today’s market is complex. But if you’re ready and able to buy right now, let’s connect to talk about how we can still make your move happen. That way you can take advantage of the long-term advantages that come with homeownership, like your ability to build wealth as your home value rises.

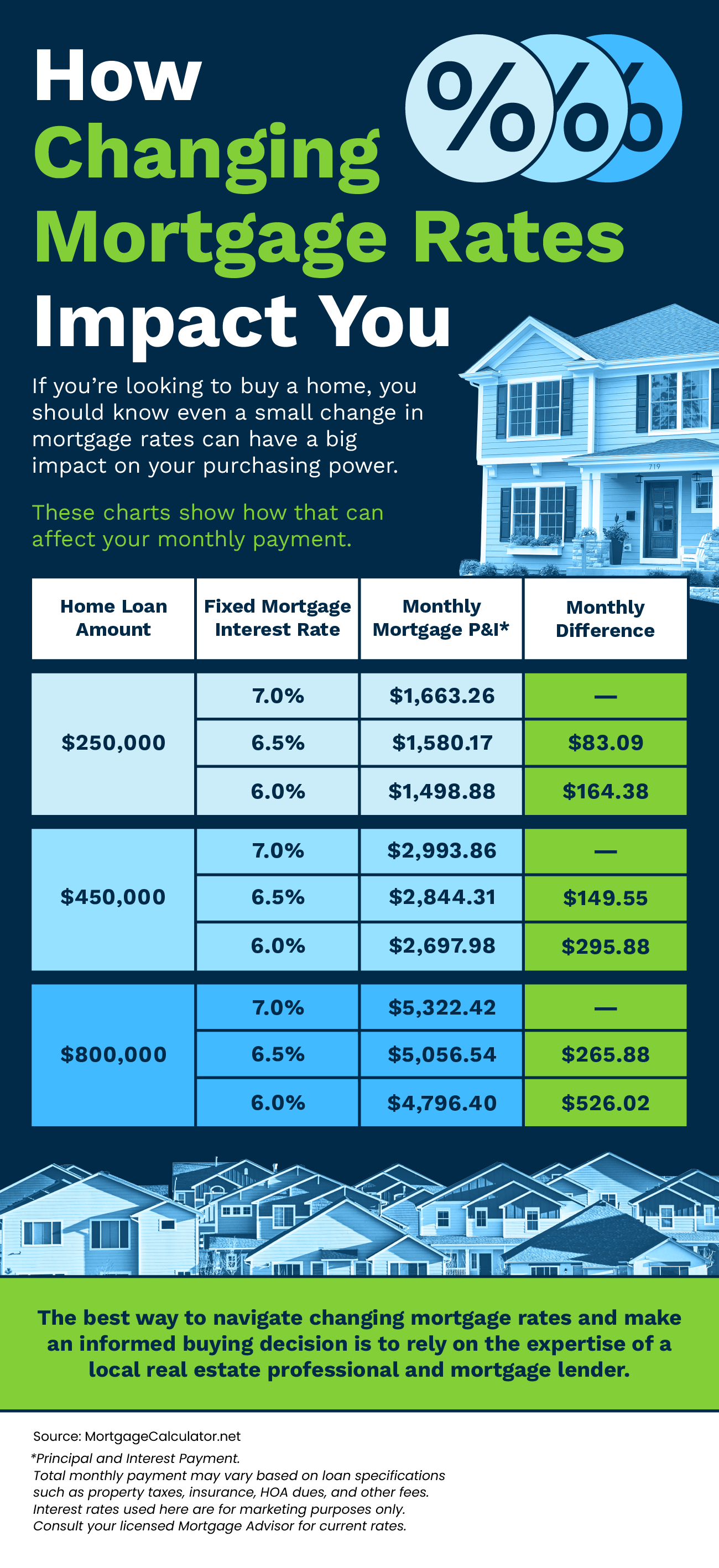

If you’ve been keeping an eye on mortgage rates lately, you might feel like you’re on a roller coaster ride. One day rates are up; the next they dip down a bit. So, what’s driving this constant change? Let’s dive into just a few of the major reasons why we’re seeing so much volatility, and what it means for you.

The Market’s Reaction to the Election

A significant factor causing fluctuations in mortgage rates is the general reaction to the political landscape. Election seasons often bring uncertainty to financial markets, and this one is no different. Markets tend to respond not only to who won, but also to the economic policies they are expected to implement. And when it comes to what’s been happening with mortgage rates over the past couple of weeks, as the National Association of Home Builders (NAHB) says:

“. . . the primary reason interest rates have been on the rise pertains to the uncertainty surrounding the presidential election. Although the election is now complete, there continue to be growing concerns over budget deficits.”

In the short term, this anticipation has caused a slight uptick in mortgage rates as the markets adjust and react. Additionally, factors like international tensions, supply chain disruptions, and trade policies can drive investor sentiment, causing them to seek safer assets like bonds, which can indirectly impact mortgage rates. Essentially, the more global or domestic uncertainty, the greater the chance that mortgage rates may shift.

The Economy and the Federal Reserve

Inflation and unemployment are two other big drivers of mortgage rates. The Federal Reserve (the Fed) has been working to bring inflation under control, and has been closely monitoring the economy as they do. And as long as inflation continues to moderate and the job market shows signs of maximum employment, the Fed will continue its plans to cut the Federal Funds Rate.

Although the Fed doesn’t set mortgage rates, their decisions do have an impact, and typically a cut leads to a mortgage rates response. And in their November 6-7th meeting, the Fed had the data they needed to make another cut to the Federal Funds Rate. And while that decision was expected and much of the mortgage rate movement happened prior to that meeting, there was a slight dip in rates.

What To Expect in the Coming Months

As we look ahead, mortgage rates will respond to changes in the Fed’s policies and other economic indicators. The markets will likely remain in a wait-and-see mode, reacting to each new development. And, with the transition of a new administration comes an element of unpredictability. A recent article from TheMortgage Reports explains:

“Today’s economic indicators come with mixed pressures on mortgage rates and we’re likely to be in for a good amount of volatility as markets adjust and respond to the election . . .”

The best way to navigate this landscape is to have a team of real estate experts by your side. Professionals will help you understand what’s happening and can provide you with the guidance you need to make informed housing market decisions along the way.

Bottom Line

The takeaway? Today’s mortgage rate volatility is going to continue to be driven by economic factors and political changes.

Now is the time to lean on experienced professionals. A trusted real estate agent and mortgage lender can help you navigate through it. And with the right guidance, you can make informed decisions.

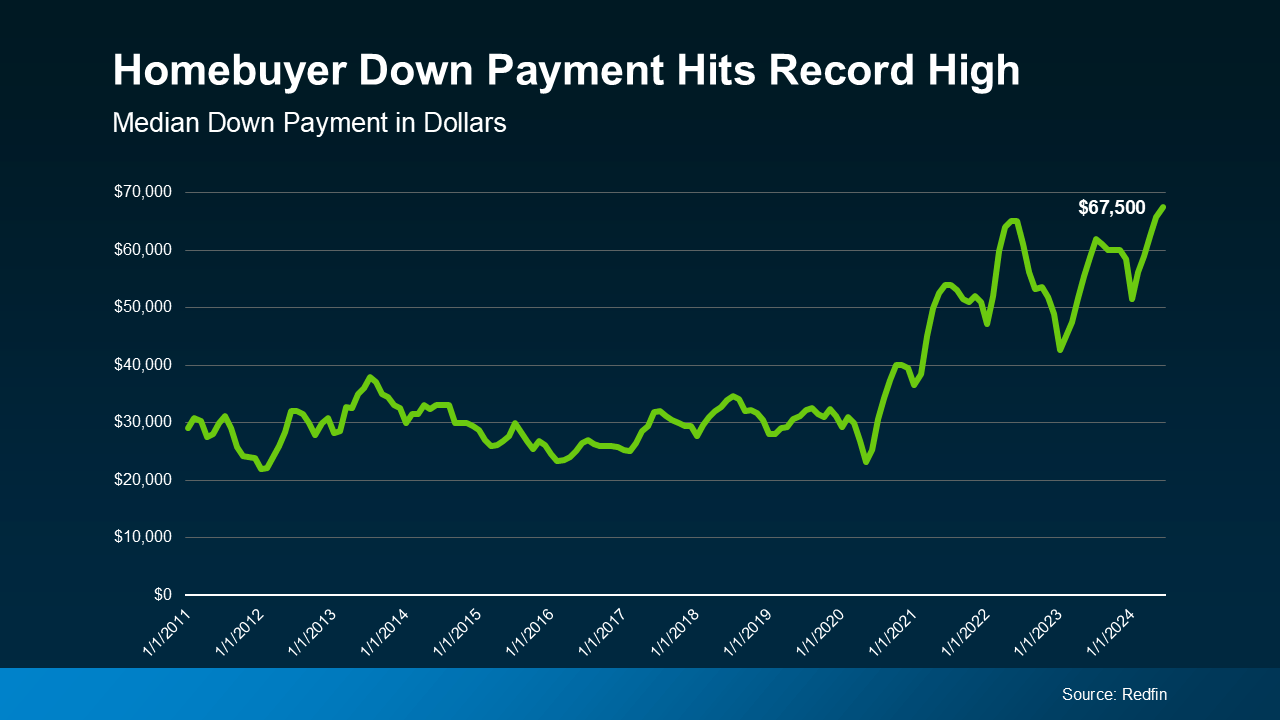

Did you know? Homeowners are often able to put more money down when they buy their next home. That’s because, once they sell, they can use the equity they have in their current house toward their next down payment. And it’s why as home equity reaches a new height, the median down payment has too.

According to the latest data from Redfin, the typical down payment for U.S. homebuyers is $67,500—that’s nearly 15% more than last year, and the highest on record (see graph below):

Here’s why equity makes this possible. Over the past five years, home prices have increased significantly, which has led to a big boost in equity for current homeowners like you. When you sell your house and move, you can take the equity that gives you and apply it toward a larger down payment on your new home. That’s a major opportunity, especially if you’ve had concerns about affordability.

Now, it’s important to remember you don’t have to make a big down payment to buy your next home—there are loan programs that let you put as little as 3%, or even 0% down. But there’s a reason so many current homeowners are opting to put more money down. That’s because it comes with some serious perks.

Why a Bigger Down Payment Can Be a Game Changer

1. You’ll Borrow Less and Save More in the Long Run

When you use your equity to make a bigger down payment on your next home, you won’t have to borrow as much. And the less you borrow, the less you’ll pay in interest over the life of your loan. That’s money saved in your pocket for years to come.

2. You Could Get a Lower Mortgage Rate

Providing a larger down payment shows your lender you’re more financially stable and not a large credit risk. The more confident your lender is in your credit score and your ability to pay your loan, the lower the mortgage rate they’ll likely be willing to give you. And that amplifies your savings.

3. Your Monthly Payments Could Be Lower

A bigger down payment doesn’t just help you reduce how much you have to borrow—it also means your monthly mortgage payment may be smaller. That can make your next home more affordable and give you a bit more breathing room in your budget.

4. You Can Skip Private Mortgage Insurance (PMI)

If you can put down 20% or more, you can avoid Private Mortgage Insurance (PMI), which is an added cost many buyers have to pay if their down payment isn’t as large. Freddie Mac explains it like this:

“For homeowners who put less than 20% down, Private Mortgage Insurance or PMI is an added insurance policy for homeowners that protects the lender if you are unable to pay your mortgage. It is not the same thing as homeowner’s insurance. It’s a monthly fee, rolled into your mortgage payment, that’s required if you make a down payment less than 20%.”

Avoiding PMI means you’ll have one less expense to worry about each month, which is a nice bonus.

Bottom Line

Down payments are at a record high, largely because recent equity gains are putting homeowners in a position to put more money down.

If you’re thinking about selling your current house and moving, let’s work together to figure out how much home equity you have right now, and how it can boost your buying power in today’s market.

If you’re thinking of making a move this year, there are two housing market factors that are probably on your mind: home prices and mortgage rates. You’re wondering what’s going to happen next. And if it’s worth it to move now, or better to wait it out.

The only thing you can really do is make the best decision you can based on the latest information available. So, here’s what experts are saying about both prices and rates.

1. What’s Next for Home Prices?

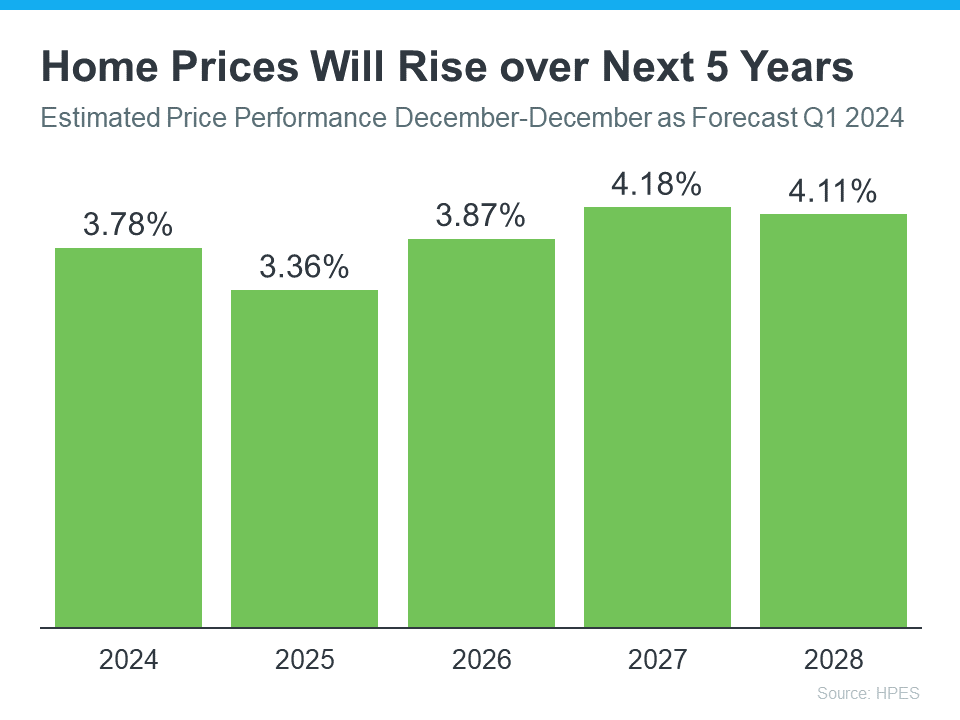

One reliable place you can turn to for information on home price forecasts is the Home Price Expectations Survey from Fannie Mae – a survey of over one hundred economists, real estate experts, and investment and market strategists.

According to the most recent release, experts are projecting home prices will continue to rise at least through 2028 (see the graph below):

While the percent of appreciation varies year-to-year, this survey says we’ll see prices rise (not fall) for at least the next 5 years, and at a much more normal pace.

What does that mean for your move? If you buy now, your home will likely grow in value and you should gain equity in the years ahead. But, based on these forecasts, if you wait and prices continue to climb, the price of a home will only be higher later on.

2. When Will Mortgage Rates Come Down?

This is the million-dollar question in the industry. And there’s no easy way to answer it. That’s because there are a number of factors that are contributing to the volatile mortgage rate environment we’re in. Odeta Kushi, Deputy Chief Economist at First American, explains:

“Every month brings a new set of inflation and labor data that can influence the direction of mortgage rates. Ongoing inflation deceleration, a slowing economy and even geopolitical uncertainty can contribute to lower mortgage rates. On the other hand, data that signals upside risk to inflation may result in higher rates.”

What happens next will depend on where each of those factors goes from here. Experts are optimistic rates should still come down later this year, but acknowledge changing economic indicators will continue to have an impact. As a CNET article says:

“Though mortgage rates could still go down later in the year, housing market predictions change regularly in response to economic data, geopolitical events and more.”

So, if you’re ready, willing, and able to afford a home right now, partner with a trusted real estate advisor to weigh your options and decide what’s right for you.

Bottom Line

Let’s connect to make sure you have the latest information available on home prices and mortgage rate expectations. Together we’ll go over what the experts are saying so you can make an informed decision on your move.

If you’re a member of a younger generation, like Gen Z, you may be asking the question: will I ever be able to buy a home? And chances are, you’re worried that’s not going to be in the cards with inflation, rising home prices, mortgage rates, and more seemingly stacked against you.

While there’s no arguing this housing market is challenging for first-time homebuyers, it is still achievable, especially if you have professionals on your side.

Here are some helpful tips you may get from a pro.

1. Explore Your Options for a Down Payment

If a down payment is your #1 hurdle, you may have options to give your savings a boost. There are over 2,000 down payment assistance programs designed to make homeownership more achievable. And, that’s not the only place you may be able to get a helping hand. While it may not be an option for everyone, 49% of Gen Z homebuyers got money from loved ones that they used toward a down payment, according to LendingTree.

And chances are you won’t need to put 20% down (unless specified by your loan type or lender). So be sure to work with a trusted mortgage professional to explore your options, find out how much you’ll really need, and learn about any guidelines on getting a gift from loved ones.

2. Live with Loved Ones To Boost Your Savings

Another thing a number of Gen Z buyers are doing is ditching their rental and moving back in with friends or family. This can help cut down your housing costs so you can build your savings a whole lot faster. As Bankrateexplains:

“. . . many have opted to stop renting and live with family in order to boost their savings. Thirty percent of Gen Z homebuyers move directly from their family member’s home to a home of their own, according to NAR.”

3. Cast a Broad Net for Your Search

When you’ve saved up enough, here’s how a pro will help you approach your search. Since the supply of homes for sale is still low and affordability is tight, they’ll give you strategies and avenues you may not have considered to open up your pool of options.

For example, it’s usually more affordable if you consider a rural or suburban area versus an urban one. So, while the city may be livelier and more energetic, the cost of living may be reason enough to look at something further out. And if you consider smaller homes and condos or townhouses, you’ll give yourself even more ways to break into the market. As Colby Stout, Research Analyst at Bright MLS, explains:

“Being flexible on the types of home (e.g., a condo or townhome versus a single-family home) and exploring more affordable neighborhoods is important for first-time buyers.”

4. Take a Close Look at Your Wants and Needs

And lastly, an agent can help you really think about your must-have’s and nice-to-have’s. Remember, your first home doesn’t have to be your forever home. You just need to get your foot in the door to start building equity. If you want to buy, you may find making some compromises is worth it. As Chase says:

“An open-minded approach to house-hunting may be one way for Gen Z homebuyers to maintain some edge. This could mean buying in areas that are less expensive. Differentiating needs vs. wants may help in this area as well.”

An agent will help you prioritize your list of home features and find houses that can deliver on the top ones. And they’ll be able to explain how equity can benefit you in the long run and make it possible to move into that dream home down the line.

Bottom Line

Real estate professionals have expertise on what’s working for other buyers like you. Lean on them for tips and advice along the way. As Directors Mortgage says,with that support you can make it happen:

“The path to homeownership may not be a straightforward one for Gen Z, but it’s undoubtedly within reach. By adopting the right strategies, like exploring down payment assistance programs and sharing living costs with relatives, you can bring your dream of owning a home closer to reality.”

Let’s connect to get you set up for long-term success.

When it comes to the current housing market, there are some myths circling around right now. Some of the more common ones are that it’s better to wait for mortgage rates to fall or prices to crash.

But there are others about the supply of homes for sale and down payments. Let’s connect so you have an expert to help separate fact from fiction in today’s housing market.

If you have student loans and want to buy a home, you might have questions about how your debt affects your plans. Do you have to wait until you’ve paid off those loans before you can buy your first home? Or is it possible you could still qualify for a home loan even with that debt? Here’s a look at the latest information so you have the answers you need.

“Roughly 60 percent of U.S. adults who have held student loan debt have put off making important financial decisions due to that debt . . . For Gen Z and millennial borrowers alone, that number rises to 70 percent.”

This includes one of the biggest financial decisions you’ll ever make, buying a home. But you should know, even with student loans, waiting to buy a home may not be necessary. While everyone’s situation is unique, your goal may be more within your reach than you realize. Here’s why.

Can You Qualify for a Home Loan if You Have Student Loans?

According to an annual report from the National Association of Realtors (NAR), 38% of first-time buyers had student loan debt and the typical amount was $30,000.

That means other people in a similar situation were able to qualify for and buy a home even though they also had student loans. And you may be able to do the same, especially if you have a steady source of income. As an article from Bankratesays:

“. . . you can have student loans and a mortgage at the same time. . . . If you have student loans and want a mortgage, there are multiple home loan programs you might qualify for . . .”

The key takeaway is, for many people, homeownership is achievable even with student loans.

You don’t have to figure this out on your own. The best way to make a decision about your goals and next steps is to talk to the professionals. A trusted lender can walk you through your options based on your situation, and share what’s worked for other buyers.

Bottom Line

Lots of other people with student loan debt are able to buy their own homes. Talk to a lender to go over your options and see how close you are to reaching your goal.

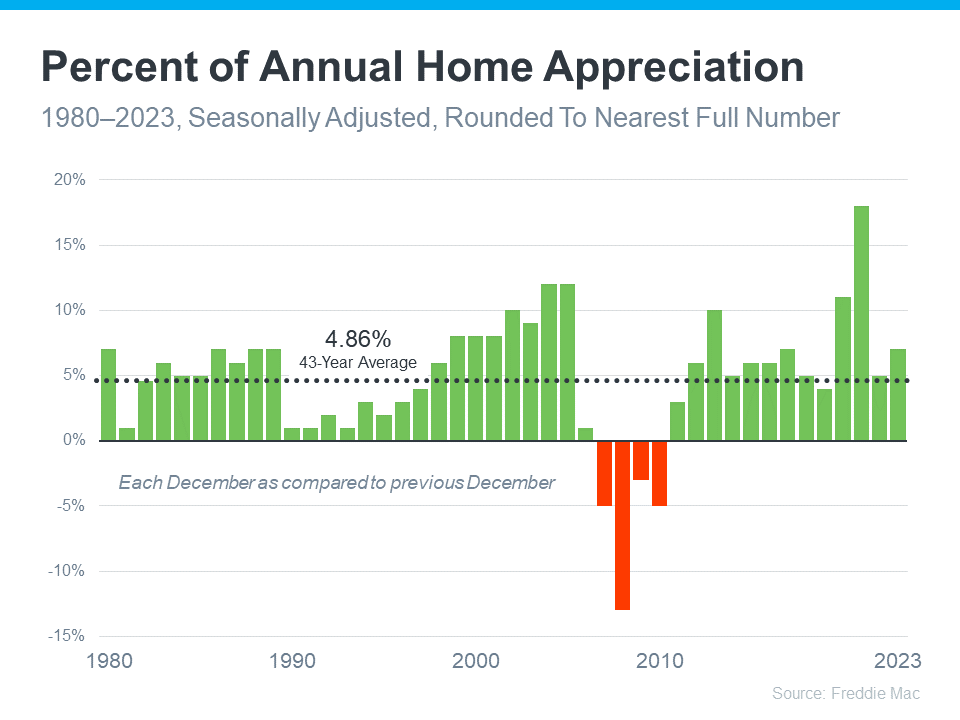

Going into 2023, there was a lot of talk about a possible recession that would cause the housing market to crash. Some in the media were even forecasting home prices would drop by as much as 10-20%—and that might have made you feel a bit unsure about buying a home.

But here’s what actually happened: home prices went up more than usual. Brian D. Luke, Head of Commodities at S&P Dow Jones Indices, explains:

“Looking back at the year, 2023 appears to have exceeded average annual home price gains over the past 35 years.”

To put last year’s growth into context, the graph below uses data from Freddie Mac on how home prices have changed each year going back to 1980. The dotted line shows the long-term average for appreciation:

“. . . the U.S. real estate market has a long and reliable history of increasing in value over time.”

In fact, since 1980, the only time home prices dropped was during the housing market crash (shown in red in the graph above). Fortunately, the market today isn’t like it was in 2008. For starters, there aren’t enough available homes to meet buyer demand right now. On top of that, homeowners have a tremendous amount of equity, so they’re on much stronger footing than they were back then. That means there won’t be a wave of foreclosures that causes prices to fall.

The fact that home values went up every single year except those four in red is why owning a home can be one of the smartest moves you can make. When you’re a homeowner, you own something that typically becomes more valuable over time. And as your home’s value appreciates, your net worth grows.

So, if you’re financially stable and prepared for the costs and expenses of homeownership, buying a home might make a lot of sense for you.

Bottom Line

Home prices almost always go up over time. That makes buying a home a smart move, if you’re ready and able. Let’s connect to talk about your goals and what’s available in our area.

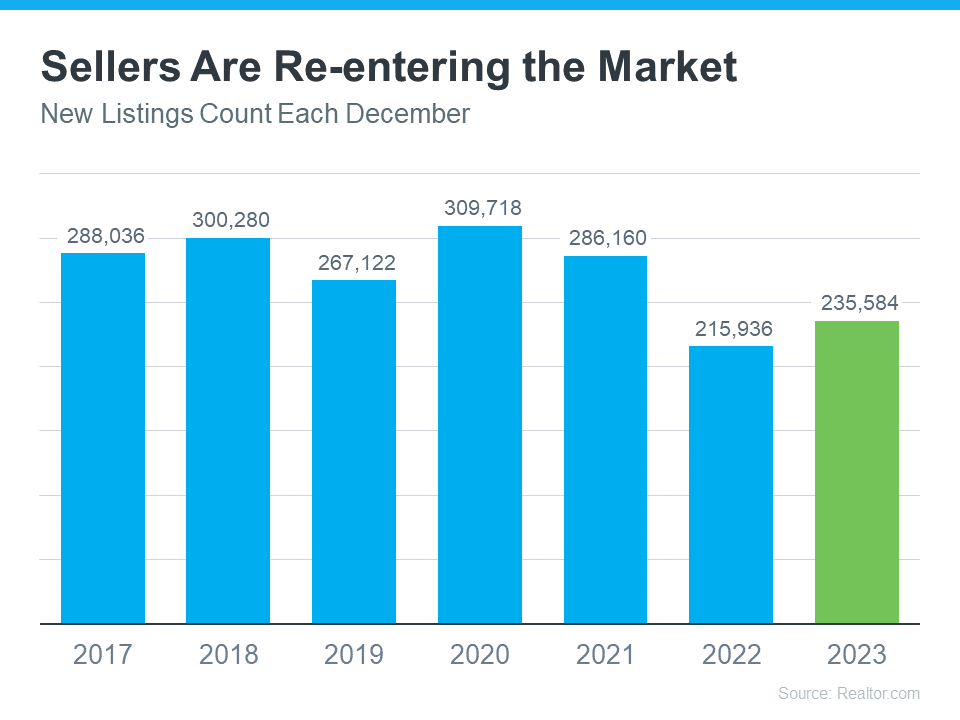

If you’re looking to buy a home, the recent downward trend in mortgage rates is good news because it helps with affordability. But there’s another way this benefits you – it may inspire more homeowners to put their houses up for sale.

The Mortgage Rate Lock-In Effect

Over the past year, one factor that’s really limited the options for your move is how few homes were on the market. That’s because many homeowners chose to delay their plans to sell once mortgage rates went up. An article from Freddie Mac explains:

“The lack of housing supply was partly driven by the rate lock-in effect. . . . With higher rates, the incentive for existing homeowners to list their property and move to a new house has greatly diminished, leaving them rate locked.”

These homeowners decided to stay put and keep their current lower mortgage rate, rather than move and take on a higher one on their next home.

Early Signs Show Those Homeowners Are Ready To Move Again

According to the latest data from Realtor.com, there were more homeowners putting their houses up for sale, known in the industry as new listings, in December 2023 compared to December 2022 (see graph below):

Here’s why this is so significant. Typically, activity in the housing market cools down in the later months of the year as some sellers choose to delay their moves until January rolls around.

This is the first time since 2020 that we’ve seen an uptick in new listings this time of year. This could be a signal that the rate lock-in effect is easing a bit in response to lower rates.

What This Means for You

While there isn’t going to suddenly be an influx of options for your home search, it does mean more sellers may be deciding to list. According to a recent article from the Joint Center for Housing Studies (JCHS):

“A reduction in interest rates could alleviate the lock-in effect and help lift homeowner mobility. Indeed, interest rates have recently declined, falling by a full percentage point from October to November 2023 . . . Further decreases would reduce the barrier to moving and give homeowners looking to sell a newfound sense of urgency . . .”

And that means you may see more homes come onto the market to give you more fresh options to choose from.

Bottom Line

As mortgage rates come down, more sellers may re-enter the market – that gives you an opportunity to find the home you’re looking for. Let’s connect so you’ve got a local expert on your side who’ll help you stay on top of the latest listings in our area.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

The second map shows that, over a roughly 30-year span, home prices appreciated by an average of more than 320% nationally.

The second map shows that, over a roughly 30-year span, home prices appreciated by an average of more than 320% nationally.