Existing-home sales across the US rose in December climbing 0.8% from the previous month and breaking a five-month streak in which sales declined, according to the National Association of REALTORS® (NAR).

Despite the increase, sales were down compared to the same period last year, as affordability challenges continued to hinder prospective buyers. Most of this period’s closed sales went under contract in October, when mortgage rates were at a two-decade high.

With rates having dropped more than a full percentage point since then, existing-home sales are forecasted to pick up in the coming months.

With average, 30-yr mortgage rates DROPPING, and inflation abating, the outlook for 2024 is positive. That being said, homebuyer demand is picking up, and without a significant increase in supply, experts believe home prices will likely remain elevated for some time to come.

NOTE: There are two photos. One is for detached homes in North county, SD and the other is for attached (condos and townhomes). If you would like specific cities or zip codes reach out to me for a more tailored synopsis.

Every buyer and seller’s situation is different and personal. Is it the right time for you to buy or list your property? Give me a call and let’s assess together. I will provide you accurate and relevant data so you can make the most informed decision possible.

If you’re thinking about buying or selling a home soon, you probably want to know what you can expect from the housing market in 2024. In 2023, higher mortgage rates, confusion over home price headlines, and a lack of homes for sale created some challenges for buyers and sellers looking to make a move. But what’s on the horizon for the new year?

The good news is, many experts are optimistic we’ve turned a corner and are headed in a positive direction.

Mortgage Rates Expected To Ease

Recently, mortgage rates have started to come back down. This has offered hope to buyers dealing with affordability challenges. Mark Fleming, Chief Economist at First American, explains how they may continue to drop:

“Mortgage rates have already retreated from recent peaks near 8 percent and may fall further . . .”

Jessica Lautz, Deputy Chief Economist at the National Association of Realtors (NAR), says:

“For home buyers who are taking on a mortgage to purchase a home and have been wary of the autumn rise in mortgage rates, the market is turning more favorable, and there should be optimism entering 2024 for a better market.”

The Supply of Homes for Sale May Grow

As rates ease, activity in the housing market should pick up because more buyers and sellers who had been holding off will jump back into action. If more sellers list, the supply of homes for sale will grow – a trend we’ve already started to see this year. Lisa Sturtevant, Chief Economist at Bright MLS, says:

“Supply will loosen up in 2024. Even homeowners who have been characterized as being ‘locked in’ to low rates will increasingly find that changing family and financial circumstances will lead to more moves and more new listings over the course of the year, particularly as rates move closer to 6.5%.”

Home Price Growth Should Moderate

And mortgage rates pulling back isn’t the only positive sign for affordability. Home price growth is expected to moderate too, as inventory improves but is still low overall.As the Home Price Expectation Survey (HPES) from Fannie Mae, a survey of over 100 economists, investment strategists, and housing market analysts,says:

“On average, the panel anticipates home price growth to clock in at 5.9% in 2023, to be followed by slower growth in 2024 and 2025 of 2.4 percent and 2.7 percent, respectively.”

To wrap it up, experts project 2024 will be a better year for the housing market. So, if you’re thinking about making a move next year, know that early signs show we’re turning a corner. As Mike Simonsen, President and Founder of Altos Research, puts it:

“We’re going into 2024 with slight home-price gains, somewhat easing inventory constraints, slightly increasing transaction volume . . . All in all, things are looking up for the U.S. housing market in 2024.”

Bottom Line

Experts are optimistic about what 2024 holds for the housing market. If you’re looking to buy or sell a home in the new year, the best way to ensure you’re up to date on the latest forecasts is to partner with a trusted real estate agent. Let’s connect.

Well, well, well…here we are already in DECEMBER! I am truly boggled as to how the holidays and the end of 2023 is among us already.

Not only am I excited for holiday lights (see below for a list of to check out) parades, hot cider and of course SANTA (!) but I’m equally excited for what is happening this week in the mortgage market. Let’s dive right in and take a look at what’s going on!

Remember, every buyer and seller’s situation is different and personal. Is it the right time for you to buy or list your property? Give me a call and let’s assess together. I will provide you accurate and relevant data so you can make the most informed decision possible.

Holiday Cheers-

Kara Brem

Real Estate News and Market Trends

November numbers are in. Here’s the scoop:

The mortgage market just had its strongest week in months and I cannot begin to explain how happy this makes me for my buyers AND sellers.

Falling mortgage rates brought increased demand as well. Total home loan applications increased 2.8% for the week ending Dec. 1 compared to the previous week, according to data from the Mortgage Bankers Association (MBA).

Slower inflation, along with the confidence financial markets have that we are nearing the end of the Fed’s hiking cycle, has brought mortgage rates to the lowest level since early August.

Now all we can do is hope that we continue to move in this direction!

Other big news is the new loan limits for 2024. In San Diego County, the Conventional limit is up to $766,550 and the high loan limit is up to $1,006,250. Most lenders begin using these new limits right away.

NOTE: There are two slides. One is for detached homes in North county, SD and the other is for attached (condos and townhomes). If you would like specific cities or zip codes reach out to me for a more tailored synopsis.

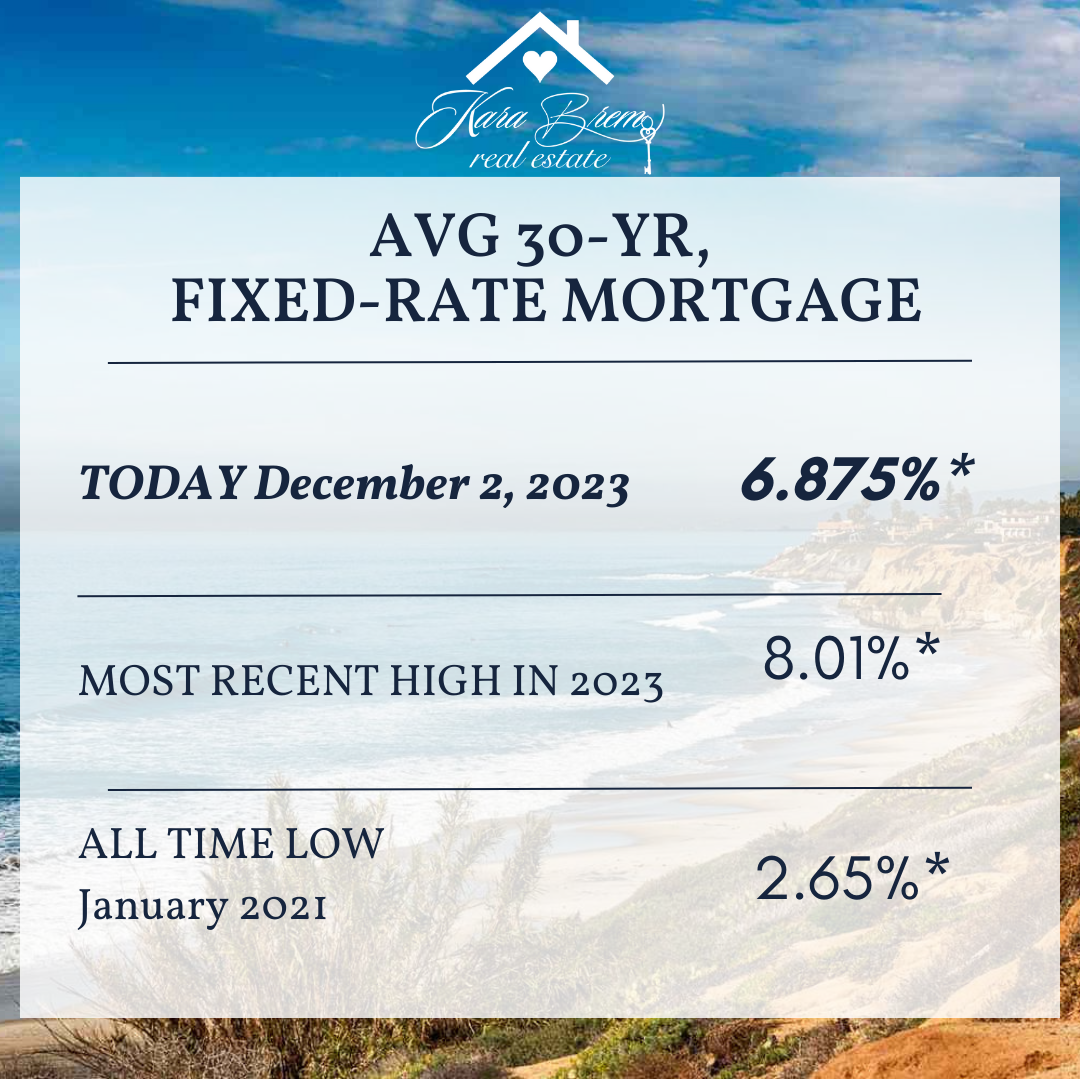

Mortgage Rate Update:

The holiday season is delivering early gifts to would-be buyers. Having climbed relentlessly for most of 2023, from just below 6% to just over 8% in October/November, average 30 year mortgage rates have plummeted in recent weeks to mid 6’s. Woohoo! Furthermore, with inflation continuing to trend lower, the markets are increasingly convinced that the Fed it’s done hiking rates and could start CUTTING rates in the first half of 2024.

It’s beginning to look a lot like Christmas. 🙂

FUN FACT: Interest rates reached their highest point in modern history in October 1981 when they peaked at 18.63%!

*No points purchased. Rates are based on 30 year fixed with excellent credit score and 20% down. This is just an estimate. Rates may vary.

If you would like to know your market value or find out if it is a good time for you to sell or buy, I am here. Reach out and let’s get started!

REALTOR®

Windermere Real Estate

DRE Lic. #01939667

Phone: 831-818-3050

Email: kara@karabrem.com

Website: www.karabrem.com

The holiday season is delivering early gifts to would-be buyers.

Having climbed relentlessly for most of 2023, from just below 6% to just over 8%, average 30 year mortgage rates have plummeted in recent weeks to mid 6’s. Woohoo! Furthermore, with inflation continuing to trend lower, the markets are increasingly convinced that the Fed it’s done hiking rates and could start CUTTING rates in the first half of 2024.

Other big news is the new loan limits for 2024. In San Diego County, the Conventional limit is up to $766,550 and the high loan limit is up to $1,006,250. Most lenders begin using these new limits right away.

It’s beginning to look a lot like Christmas. 🙂

*No points purchased. Rates are based on 30 year fixed with excellent credit score and 20% down. This is just an estimate. Rates may vary.

.

.

.

Kara Brem REALTOR®

DRE Lic. #01939667

(831) 818-3050

kara@karabrem.com

Signs that your neighborhood is about to POP and your property values are about to skyrocket 🚀

*Whole Foods/Starbucks/Target moves in*

Studies have proven that neighborhood amenities have a direct impact on property values. When household-name brands set up shop in your community, it’s usually a good sign as those companies are researching way ahead of time where to go next. Often times their research teams know better than any of us where the next up and coming areas are. These amenities bring traffic into the neighborhood and jobs to the local economy, and make the area more convenient and attractive to prospective buyers.

*Local school scores are increasing*

Whether or not there are children in your family or future, local school scores definitely impact resale value. San Diego is home to some of the best private and public schools in the state and has an inarguable impact on local property values.

*Planter boxes and flower beds start cropping up*

Do your neighbors take pride in maintaining their homes? Do you have a tight-knit community where neighbors look out for each other? Believe it or not, neighborhood pride can increase property values. Property maintenance can be indicative of what your lifestyle will be like in a specific neighborhood, both for you as a homeowner and for future prospective buyers who would rather see a well-manicured lawn and flower pots on the front porch than peeling paint and broken front steps.

*A major corporation sets up headquarters nearby*

When big businesses move to town, they not only bring jobs but also head count. If you have an influx of people moving into your community, there’s going to be more competition for existing homes and possibly more development opportunities for local investors. Not to mention, big corporations want to entice workers and tend to give back to make their surrounding communities a comfortable place to live.

Questions about property values in your neighborhood? Reach out anytime and we can schedule a casual coffee or quick phone call!

The following analysis of select counties of the Southern California real estate market is provided by Windermere Real Estate Chief Economist Matthew Gardner. I hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact me.

Regional Economic Overview

The Southern California market areas contained in this report have been experiencing a fairly significant slowdown in job growth. That said, the region has added 164,700 jobs since the third quarter of 2022, representing a growth rate of 1.7%. The end of the writers’ strike will add a little boost to the Los Angeles area, which has still added over 89,000 jobs over the past 12 months. Orange County employment has grown by 34,100 jobs; San Diego County is higher by 31,400; and employment was up 9,700 jobs in Riverside.

The region’s unemployment rate in August was 5.2%, which was up from 4.2% in the third quarter of 2022. The lowest jobless rate was in San Diego County, where it was 4.3%. The highest rate was in Los Angeles County, where 5.8% of the workforce was without a job.

Southern California Home Sales

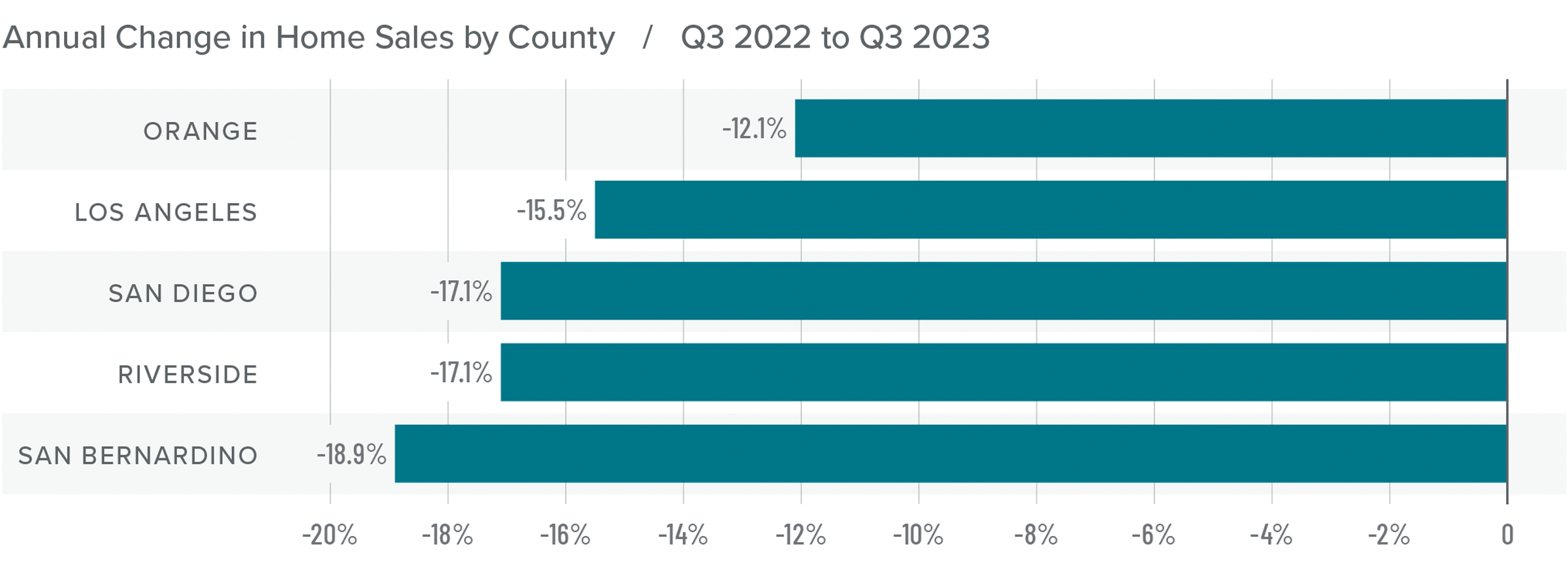

❱ In the third quarter of 2023, 32,398 homes sold, which was 16% lower than in the third quarter of 2022 and down 8.6% compared to the second quarter of this year.

❱ Pending home sales, which are an indicator of future closings, were 8.2% lower than in the second quarter, suggesting that closing numbers may be down in the final quarter of 2023.

❱ Compared to the third quarter of 2022, sales fell the most in San Bernardino County, though there was a significant decline in all markets. The quarter-over-quarter decline was disconcerting given that the number of homes for sale rose more than 14%. Rising mortgage rates are clearly taking their toll on the market.

❱ It’s discouraging that there were fewer sales despite rising inventory levels. Mortgage rates are definitely hobbling the market and until they start to drop, I think things will continue to be lackluster. List prices have started to pull back in response, as sellers realize that the market is not what it once was.

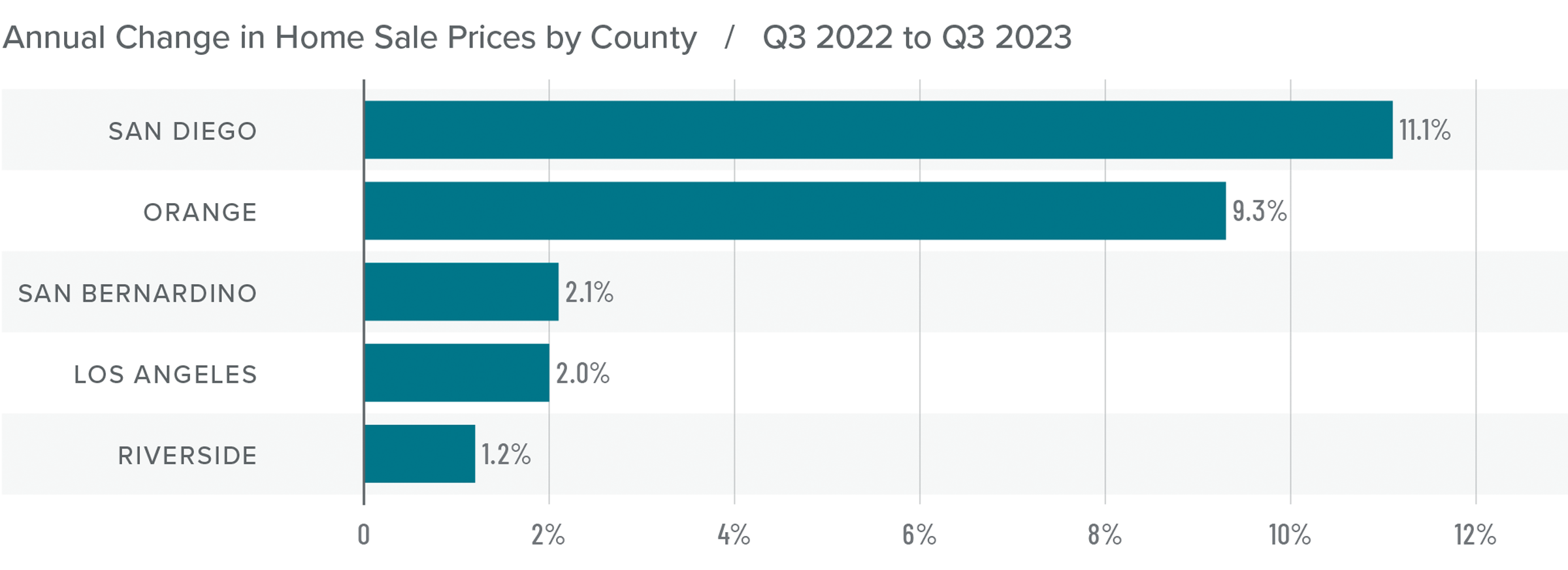

Southern California Home Prices

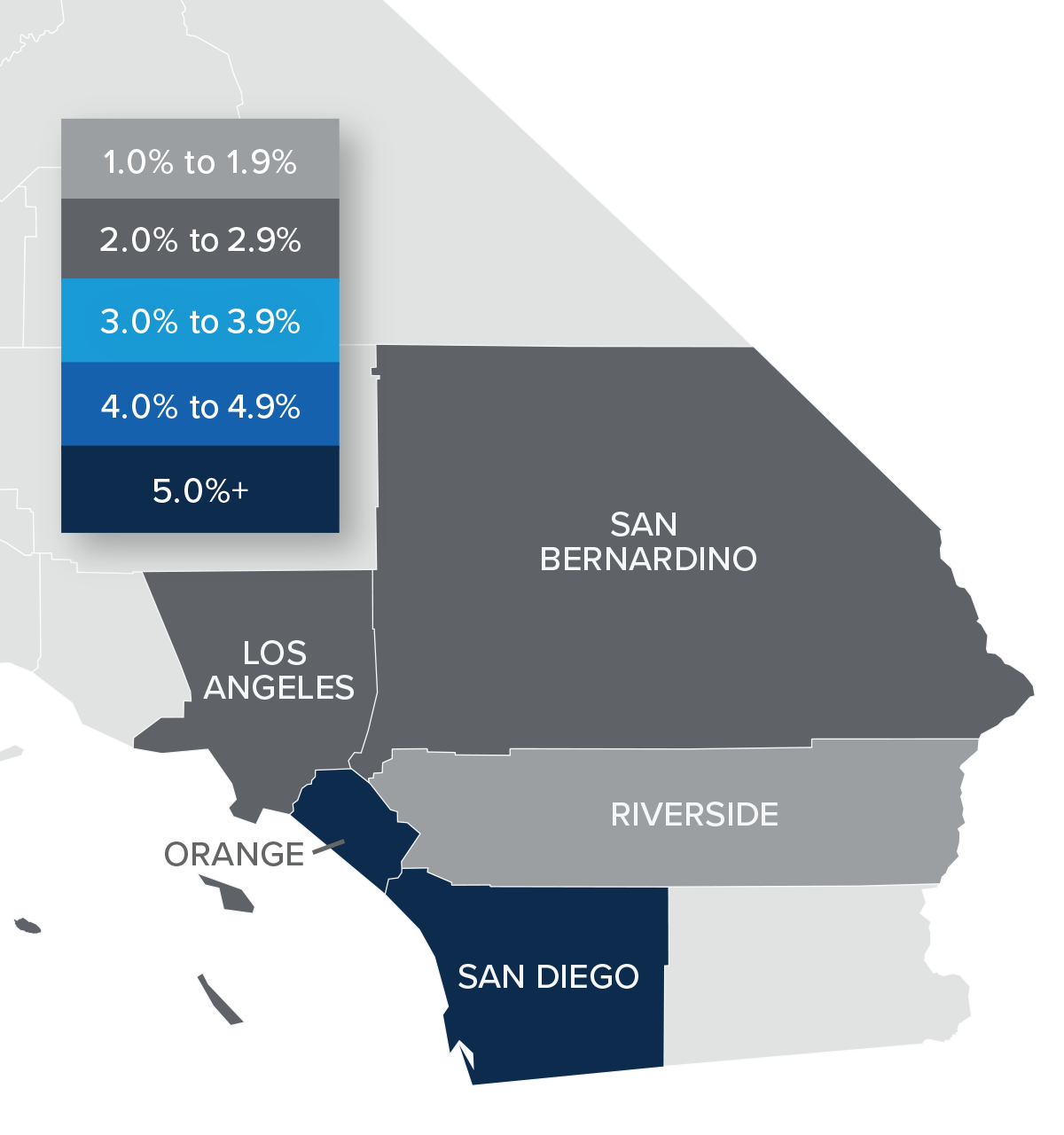

❱ Home sale prices were up 5.7% from the third quarter of 2022 and were 3.8% higher than in the second quarter of 2023.

❱ Affordability continues to be a major constraint in the region, which is being magnified by persistently high mortgage rates. Prices are holding, but growth has slowed significantly.

❱ Year over year, prices rose in all the markets contained in this report, with significant increases in San Diego and Orange counties. Compared to the second quarter of 2023, Riverside County saw prices fall by 5.8%, but they rose in the balance of the market areas.

❱ I expect price growth in Southern California to hold at or near the current pace. However, it’s very possible that home sale prices could drop a little if list prices fall further.

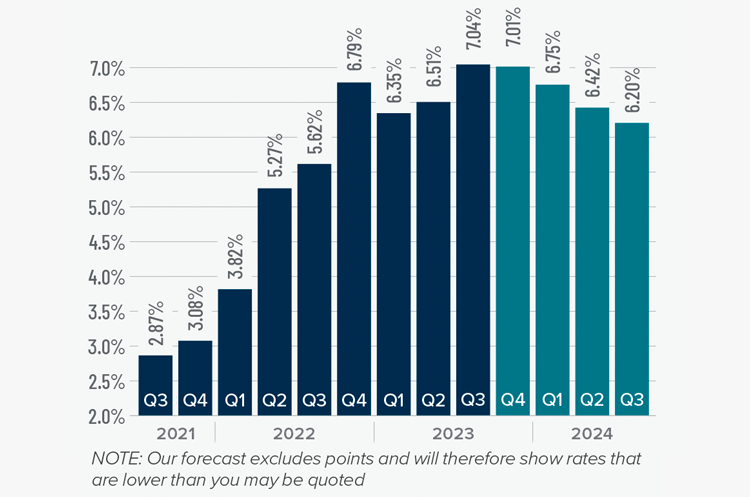

Mortgage Rates

Mortgage rates continued trending higher in the third quarter of 2023 and are now at levels we have not seen since the fall of 2000. Mortgage rates are tied to the interest rate (yield) on 10-year treasuries, and they move in the opposite direction of the economy. Unfortunately for mortgage rates, the economy remains relatively buoyant, and though inflation is down significantly from its high, it is still elevated. These major factors and many minor ones are pushing Treasury yields higher, which is pushing mortgage rates up. Given the current position of the Federal Reserve, which intends to keep rates “higher for longer,” it is unlikely that home buyers will get much reprieve when it comes to borrowing costs any time soon.

With such a persistently positive economy, I have had to revise my forecast yet again. I now believe rates will hold at current levels before starting to trend down in the spring of next year.

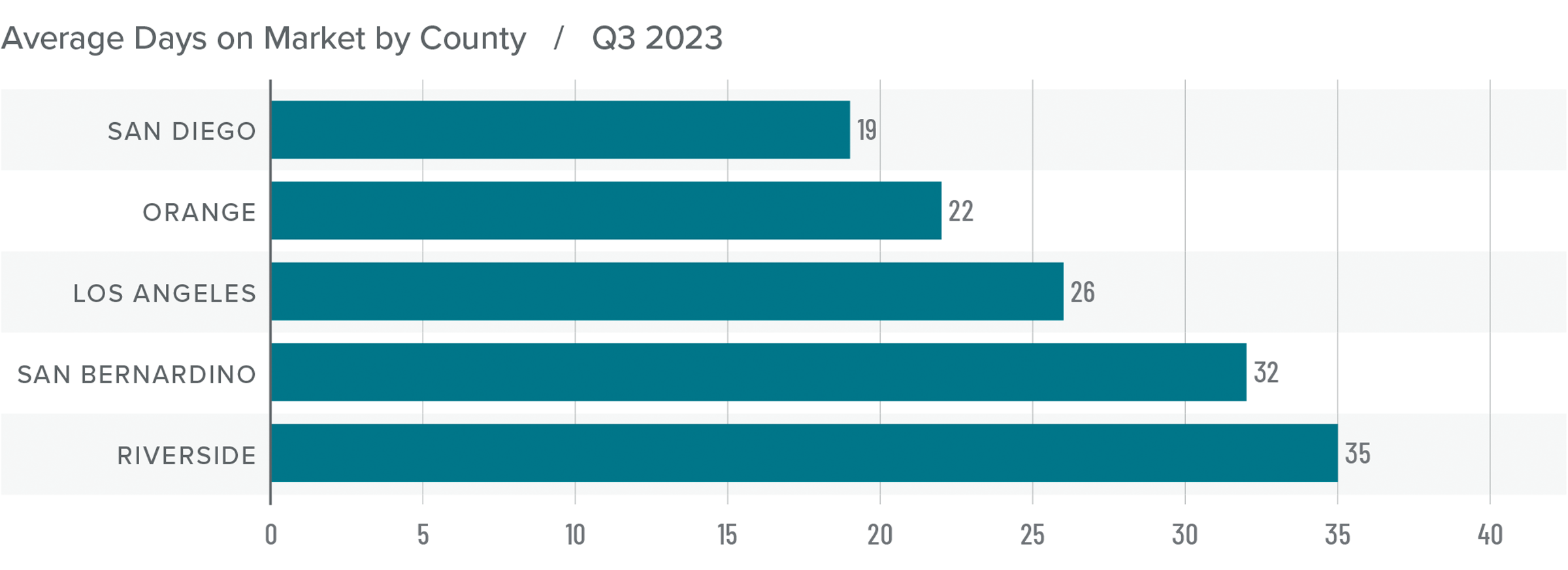

Southern California Days on Market

❱ In the third quarter of 2023, the average time it took to sell a home in the region was 27 days. This was up two days compared to the same period of 2022.

❱ Compared to the second quarter of 2023, market time fell six days and was lower across all counties covered by this report.

❱ Homes in San Diego County continue to sell at a faster rate than other markets in the region, but it took two fewer days to sell a home than it did in the third quarter of 2022. Orange County saw days on market fall by one day compared to the third quarter of 2022, but market time rose everywhere else.

❱ Homebuyers saw rising inventories, and those who chose to make offers did so relatively quickly, even though the total number of sales fell. If the number of homes for sale continues to rise, it may also cause market time to rise as buyers become more selective.

Conclusions

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

With inventory levels rising, and sales and asking prices falling, it would be easy to suggest that home buyers have the upper hand. However, home prices are still rising, albeit slowly, which tends to favor sellers.

The quandary really comes down to the fact that while inventory levels have risen, they remain remarkably low compared to historic averages. It’s also likely that the buyers who are still in the market are looking to move more from necessity than desire, which makes sense given today’s high mortgage rates.

That has put us in a very unusual situation. Although sellers are being a little more competitive, as evidenced by the drop in list prices, they have not totally capitulated. Taking all these factors into consideration, I have moved the needle back to the middle of the speedometer. I simply don’t see either side as having the upper hand at the present time.

About Matthew Gardner

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

Mortgage rates have been back on the rise recently and that’s getting a lot of attention from the press. If you’ve been following the headlines, you may have even seen rates recently reached their highest level in over two decades (see graph below):

That can feel like a little bit of a gut punch if you’re thinking about making a move. If you’re wondering whether or not you should delay your plans, here’s what you really need to know.

How Higher Mortgage Rates Impact You

There’s no denying mortgage rates are higher right now than they were in recent years. And, when rates are up, that affects overall home affordability. It works like this. The higher the rate, the more expensive it is to borrow money when you buy a home. That’s because, as rates trend up, your monthly mortgage payment for your future home loan also increases.

Urban Instituteexplains how this is impacting buyers and sellers right now:

“When mortgage rates go up, monthly housing payments on new purchases also increase. For potential buyers, increased monthly payments can reduce the share of available affordable homes . . . Additionally, higher interest rates mean fewer homes on the market, as existing homeowners have an incentive to hold on to their home to keep their low interest rate.”

Basically, some people are deciding to put their plans on hold because of where mortgage rates are right now.But what you want to know is: is that a good strategy?

Where Will Mortgage Rates Go from Here?

If you’re eager for mortgage rates to drop, you’re not alone. A lot of people are waiting for that to happen. But here’s the thing. No one knows when it will. Even the experts can’t say with certainty what’s going to happen next.

Forecasts project rates will fall in the months ahead, but what the latest data says is that rates have been climbing lately. This disconnect shows just how tricky mortgage rates are to project.

The best advice for your move is this: don’t try to control what you can’t control. This includes trying to time the market or guess what the future holds for mortgage rates. As CBS Newsstates:

“If you’re in the market for a new home, experts typically recommend focusing your search on the right home purchase — not the interest rate environment.”

Instead, work on building a team of skilled professionals, including a trusted lender and real estate agent, who can explain what’s happening in the market and what it means for you. If you need to move because you’re changing jobs, want to be closer to family, or are in the middle of another big life change, the right team can help you achieve your goal, even now.

Bottom Line

The best advice for your move is: don’t try to control what you can’t control – especially mortgage rates. Even the experts can’t say for certain where they’ll go from here. Instead, focus on building a team of trusted professionals who can keep you informed. When you’re ready to get the process started, let’s connect.

You might remember the housing crash in 2008, even if you didn’t own a home at the time. If you’re worried there’s going to be a repeat of what happened back then, there’s good news – the housing market now is different from 2008.

One important reason is there aren’t enough homes for sale. That means there’s an undersupply, not an oversupply like the last time. For the market to crash, there would have to be too many houses for sale, but the data doesn’t show that happening.

Housing supply comes from three main sources:

Homeowners deciding to sell their houses

Newly built homes

Distressed properties (foreclosures or short sales)

Here’s a closer look at today’s housing inventory to understand why this isn’t like 2008.

Homeowners Deciding To Sell Their Houses

Although housing supply did grow compared to last year, it’s still low. The current months’ supply is below the norm. The graph below shows this more clearly. If you look at the latest data (shown in green), compared to 2008 (shown in red), there’s only about a third of that available inventory today.

So, what does this mean? There just aren’t enough homes available to make home values drop. To have a repeat of 2008, there’d need to be a lot more people selling their houses with very few buyers, and that’s not happening right now.

Newly Built Homes

People are also talking a lot about what’s going on with newly built houses these days, and that might make you wonder if homebuilders are overdoing it. The graph below shows the number of new houses built over the last 52 years:

The 14 years of underbuilding (shown in red) is a big part of the reason why inventory is so low today. Basically, builders haven’t been building enough homes for years now and that’s created a significant deficit in supply.

While the final blue bar on the graph shows that’s ramping up and is on pace to hit the long-term average again, it won’t suddenly create an oversupply. That’s because there’s too much of a gap to make up. Plus, builders are being intentional about not overbuilding homes like they did during the bubble.

Distressed Properties (Foreclosures and Short Sales)

The last place inventory can come from is distressed properties, including short sales and foreclosures. Back during the housing crisis, there was a flood of foreclosures due to lending standards that allowed many people to get a home loan they couldn’t truly afford.

Today, lending standards are much tighter, resulting in more qualified buyers and far fewer foreclosures. The graph below uses data from the Federal Reserve to show how things have changed since the housing crash:

This graph illustrates, as lending standards got tighter and buyers were more qualified, the number of foreclosures started to go down. And in 2020 and 2021, the combination of a moratorium on foreclosures and the forbearance program helped prevent a repeat of the wave of foreclosures we saw back around 2008.

The forbearance program was a game changer, giving homeowners options for things like loan deferrals and modifications they didn’t have before. And data on the success of that program shows four out of every five homeowners coming out of forbearance are either paid in full or have worked out a repayment plan to avoid foreclosure. These are a few of the biggest reasons there won’t be a wave of foreclosures coming to the market.

What This Means for You

Inventory levels aren’t anywhere near where they’d need to be for prices to drop significantly and the housing market to crash. According to Bankrate, that isn’t going to change anytime soon, especially considering buyer demand is still strong:

“This ongoing lack of inventory explains why many buyers still have little choice but to bid up prices. And it also indicates that the supply-and-demand equationsimply won’t allow a price crash in the near future.”

Bottom Line

The market doesn’t have enough available homes for a repeat of the 2008 housing crisis – and there’s nothing that suggests that will change anytime soon. That’s why housing inventory tells us there’s no crash on the horizon.

One question that’s top of mind if you’re thinking about making a move today is: Why is it so hard to find a house to buy? And while it may be tempting to wait it out until you have more options, that’s probably not the best strategy. Here’s why.

There aren’t enough homes available for sale, but that shortage isn’t just a today problem. It’s been a challenge for years. Let’s take a look at some of the long-term and short-term factors that have contributed to this limited supply.

Underbuilding Is a Long-Standing Problem

One of the big reasons inventory is low is because builders haven’t been building enough homes in recent years. The graph below shows new construction for single-family homes over the past five decades, including the long-term average for housing units completed:

For 14 straight years, builders didn’t construct enough homes to meet the historical average (shown in red). That underbuilding created a significant inventory deficit. And while new home construction is back on track and meeting the historical average right now, the long-term inventory problem isn’t going to be solved overnight.

Today’s Mortgage Rates Create a Lock-In Effect

There are also a few factors at play in today’s market adding to the inventory challenge. The first is the mortgage rate lock-in effect. Basically, some homeowners are reluctant to sell because of where mortgage rates are right now. They don’t want to move and take on a rate that’s higher than the one they have on their current home. The chart below helps illustrate just how many homeowners may find themselves in this situation:

Those homeowners need to remember their needs may matter just as much as the financial aspects of their move.

Misinformation in the Media Is Creating Unnecessary Fear

Another thing that’s limiting inventory right now is the fear that’s been created by the media. You’ve likely seen the negative headlines calling for a housing crash, or the ones saying home prices would fall by 20%. While neither of those things happened, the stories may have dinged your confidence enough for you to think it’s better to hold off and wait for things to calm down. As Jason Lewris, Co-Founder and Chief Data Officer at Parcl, says:

“In the absence of trustworthy, up-to-date information, real estate decisions are increasingly being driven by fear, uncertainty, and doubt.”

That’s further limiting inventory because people who would make a move otherwise now feel hesitant to do so. But the market isn’t doom and gloom, even if the headlines are. An agent can help you separate fact from fiction.

How This Impacts You

If you’re wondering how today’s low inventory affects you, it depends on if you’re selling or buying a home, or both.

For buyers: A limited number of homes for sale means you’ll want to seriously consider all of your options, including various areas and housing types. A skilled professional will help you explore all of what’s available and find the home that best fits your needs. They can even coach you through casting a broader net if you need to expand your search.

For sellers: Today’s low inventory actually offers incredible benefits because your house will stand out. A real estate agent can walk you through why it’s especially worthwhile to sell with these conditions. And since many sellers are also buyers, that agent is also an essential resource to help you stay up to date on the latest homes available for sale in your area so you can find your next dream home.

Bottom Line

The low supply of homes for sale isn’t a new challenge. There are a number of long-term and short-term factors leading to the current inventory deficit. If you’re looking to make a move, let’s connect. That way you’ll have an expert on your side to explain how this impacts you and what’s happening with housing inventory in our area.

Happy August everyone (or shall we say Fogust?). The real estate market and mortgage rates continue to keep all of us in related fields scratching our heads. So if you are confused…not to worry. It’s not just you. Let’s dive right in and take a look at what’s going on in our local area.

Remember, every buyer and seller’s situation is different and personal. Is it the right time for you to buy or list your property? Give me a call and let’s assess together. I will provide you accurate and relevant data so you can make the most informed decision possible.

Cheers-

Kara Brem

Real Estate News and Market Trends

July numbers are in. Here’s the scoop:

Affordability constraints have continued to limit home buying activity this summer with mortgage rates wobbling back and forth in the high 6’s and recently hitting 7% again leading many prospective buyers to put their home purchase plans temporarily on hold.

Higher rates have also kept many existing homeowners from listing their homes for fear of giving up the low-rate mortgages they locked in a few years ago, when rates were significantly lower. This fuels our ongoing limited inventory issue.

Despite a drop in existing-home sales, home prices have remained near record highs and limited inventory has boosted competition among buyers, putting upward pressure on sales prices, especially in more affordable markets and highly desirable markets (like North County SD), where competition for

homes remains particularly strong.

* Note two images…one for detached homes in North county, SD and the other for attached (condos and townhomes). If you would like specific cities or zip codes reach out to me for a more tailored synopsis.

Mortgage rate update:

Still a bit of a rollercoaster in mortgage rate land. We were moving lower a few weeks ago and then popped back up to above 7% early August. End of last week we were down to 6.75% and as of yesterday we are back up to 7.15%!

Buyers are adjusting to this new rate norm and we’re starting to see those that are tired of sitting on the fence move forward with purchasing plans. Date the rate, marry the house. You can always refinance when rates drop. But remember…if rates do go down (and we’re not certain they will go that much lower) you will also be joining all the buyers that have been waiting to purchase this last year which COULD increase home prices again.

*No points purchased. Rates are based on 30 year fixed with excellent credit score and 20% down. This is an estimate. Rates may vary.

There you have it. Data driven market insights with real numbers. If you’re considering buying or selling in teh next 9 months or so, give me a call and let’s get started!

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link