When it comes time to sell your home, determining its exact value can be a challenge. Naturally, homeowners want to get the most value for their home. However, if it hits the market at too high a price, it could cause serious complications in the selling process.

Attracting the wrong buyers

An overpriced home creates a kind of seller’s limbo that draws the attention of the wrong buyers, which is a surefire way to start your selling process off on the wrong foot.

A vast majority of homebuyers begin their home search online, especially during these days of social distancing amidst the COVID-19 pandemic. If your home is overpriced in comparison to other listings in your area, it won’t appear in their search results. In this way, an overpriced home is blind to its intended buyers and actually drives traffic to nearby listings that are more accurately priced.

An overpriced home can’t compete with listings in a more expensive bracket. Buyers know what they want, and they know what to expect in their price range. When they notice a home is missing the square footage, features, and amenities typically found in others at the same price, they will quickly lose interest.

Fewer showings / virtual tours

Showings—both physical and virtual—play a significant role in the sale of your home. They give buyers a first-hand look and provide them the opportunity to ask questions and gather more information. Selling your home is a numbers game. The more showings scheduled at your listing, the more potential buyers you have. The more potential buyers, the greater chance of an offer.

Your agent knows that showings are critical to capturing buyer interest. But if the home is overpriced, they will have difficulty attracting attention to your home. This can slow the entire home selling process, leaving both the seller and agent feeling frustrated.

Expired shelf life

Think of the home you’re selling as a fresh tomato. Off the vine (newly listed), it is fresh and attractive, appealing to everyone in the market and standing out amongst the other tomatoes. As time goes on, no one buys the tomato and it begins to overripen and wither, losing its appeal. This is what happens to an overpriced home in the minds of buyers.

New listings attract the most attention—that’s when buyer interest is highest. The longer your home is on the market, the less appealing it becomes. At a certain point, sellers are forced to lower the price. However, this lowered price won’t have the same impact as hitting the market correctly priced the first time. Once price drops begin, they can continue, which creates the risk of selling the home for less than what it is worth.

Lastly, the longer your home is on the market, the more expenses you incur. Mortgage payments, utilities costs and seller’s fees will continue to pile up, making it harder to recover from these costs when your home does eventually sell.

Post-sale complications

Let’s say you do find a buyer at the overpriced cost. During closing, the lender will order an appraisal of your home, and if the appraiser finds that the market value of the home is less than the selling price, they could potentially deny financing.

Talk to your Windermere agent about how to price your home correctly to avoid these pitfalls of overpricing. Knowing your home’s worth will set you up for success when it comes time to hit the market.

Posted September 9 2020, 11:00 AM PDT by Sandy Dodge

Contrary to popular belief, going green does not have to be hard or cost money, in fact it can even save you money. There are many small things that you and your family can do within your home to save money while reducing landfill waste and the use of natural resources. Discover a few ways to go green and save some money by choosing a green home.

Compost Bin

Composting is free and can provide you with rich soil to garden with. You will never have to buy soil and can easily grow plants and vegetables. To create your own bin, get a large trashcan with a locking lid, then drill about 25 holes all around the bin and attach the bin to small platform (allows it to drain). Once you start putting approved items in the bin go outside and roll it around in the grass every few days.

Energy Efficient Light Bulbs

You can save approximately $75 dollars a year by replacing your traditional incandescent with energy efficient light bulbs. On average energy efficient light bulbs typically use way less energy and can last much longer, not needing to be replaced as much.

Laundry

There are quite a few options to save money and energy when it comes to laundry. Here are a few: wait till you have a full load of laundry to wash, line dry your clothes, wash your clothes in cold water and when it comes time to get a new washer and dryer buy an energy efficient one.

Weather-Strip & Caulk

One of the main ways we use a lot of energy, especially in hot and cold climates, is through air-conditioning and heating. One way to reduce the use of heating and air-conditioning is to properly weather strip and caulk all windows and doors keeping your home cool and warm when needed.

Reuse and Reduce

Use items more than once when you can to avoid throwing them out; this might mean buying quantity over quality. Another way is to join The Freecycle Network or Buy Nothing group on Facebook you can swap used goods with neighbors for free and also keeping more waste out of landfills.

DIY Cleaning

Start making your own cleaning products. Not only can you customize, make them eco-friendlier but you will also save money buying products. On average, most DIY cleaners cost less than a $1 to make per bottle compared to $5-$15 per store bought bottle.

Unplug & Turn Off

Put all your major electronics on a power strip and shut off when they are not in use. Even if your electronics are shut off, they still will continue to draw electricity thought out the day. Another tip is to make sure you unplug your cellphone when completely charged and always power everything down while not in use to save on battery life.

Toilet

There is an extremely easy way to make your toilet a low flow toilet. Simply add a brick, wrapped in a waterproof bag or take a plastic water bottle and fill it with sand putting it into your tank. This will reduce the amount of water with every flush. Once you are ready for a new toilet purchase a low-flush toilet.

Shower

Change up your shower head with an energy-efficient shower head that will use half the amount of water. These shower heads are low flow but will significantly cut your water bill down. Another option is to install a tap aerator which will also cut down water usage without changing the water pressure.

Mortgage rates dropped to a record low last week, averaging 2.86 percent for a 30-year fixed-rate loan. This marks the ninth time in 2020 that mortgage rates have hit a new floor. At the same time, mortgage credit availability shrunk to a six-year low in August, meaning lending standards have tightened.

Buyer demand still remains high, with mortgage applications up 40 percent from a year ago. California REALTORS® surveyed by C.A.R. reported encouraging business results last week, though optimism about future slides slipped modestly.

Demand continues to surge in “Zoom towns,” smaller, more affordable markets outside of bigger metropolitan areas that have become more popular as more people have been working remotely. A new study from Zillow found that nearly 2 million American renters could become homebuyers if they were able to work remotely and move to a less expensive area.

Meanwhile, the number of homes for sale nationwide is in record low territory, with some of the more affordable areas seeing the biggest drops in inventories. In Q2 2020, iBuying activity on the part of RedfinNow, Offerpad, Opendoor and Zillow plummeted 88 percent. But now, with activity resumed, Opendoor is reportedly in talks to go public through a merger with Social Capital Hedosophia Holdings Corp. II, a company that acquires other companies in order to take them public.

Sources: MSN Money, REALTOR® Magazine, C.A.R. Research & Economics, NPR, Inman News, Mortgage Professionals of America, HousingWire, Redfin

The year 2020 will certainly be one to remember, with new realities and norms that changed the way we live. This year’s real estate market is certainly no exception to that shift, with historic highlights continuing to break records and challenge what many thought possible in the housing market. Here’s a look at four key areas that are fundamentally defining the market this year.

Housing Market Recovery

The economy was intentionally put on pause this spring in response to the COVID-19 health crisis. Many aspects of the common real estate transaction were placed on hold at the same time. Thankfully, technology and innovation helped the industry power forward, and business gradually ramped back up as shelter-in-place orders were lifted.

The result? Total transformation of the market from rock-bottom lows to exceptional highs. Today, the housing recovery is being called truly remarkable by many experts and is far exceeding expectations. From pending home sales to purchase applications, buyers are back in business and homes are selling – fast.

According to the Housing Market Recovery Index by realtor.com, the market has surpassed pre-pandemic levels, and has regained the strength we remember from February of this year (See graph below):

Record-Breaking Mortgage Rates

Historically low mortgage rates are another 2020 game-changer. Today’s low rate is one of the big motivating factors bringing buyers back into the market. The average rate reached an all-time low on multiple occasions this year, and it continues to hover in record-low territory.

When rates are this low, buyers have a huge opportunity to get more for their money when purchasing a home, something many are eager to find while continuing to spend more time than expected at home this year, and likely beyond.

Continued Home Price Appreciation

One of the key drivers of home price appreciation this year is historically low inventory. Inventory was low going into the pandemic, and it is still sitting well below the level needed for a normal market. Although sellers are slowly making their way back into the game, buyers are scooping up homes faster than they’re coming up for sale.

This is a classic supply and demand scenario, forcing home prices to rise. Selling something when there is a higher demand for what is available naturally bumps up the price. If you’re ready to sell your house today, this may be the optimal time to make your move. As Bill Banfield, EVP of Capital Markets at Quicken Loans, notes:

“The pandemic has not stopped the consistent home price growth we have witnessed in recent years.”

Increasing Affordability

Even as home prices continue to rise, affordability is working in favor of today’s homebuyers. According to many experts, rates this low are off-setting rising home prices, which increases buyer purchasing power – an opportunity not to be missed, especially if your family’s needs have changed. If you now need space for a home office, gym, virtual classroom, and more, it may be time to reconsider your current house.

“Those shopping for a home can afford 10 percent more home than they could have one year ago while keeping their monthly payment unchanged. This translates into nearly $32,000 more buying power.”

Bottom Line

With mortgage rates hitting historic lows, home prices appreciating, affordability rising, and the market recovering like no other, 2020 has been quite a year for real estate – perhaps one we’ve never seen before and may never see again. Let’s connect today if you’re ready to take advantage of this year’s record-breaking opportunities.

For homeowners looking to reduce their home’s carbon footprint, increase its sustainability, and add value to their property, going solar is an obvious choice. Understanding how solar works and how to maximize its benefits are key first steps in your journey to becoming a solar energy-producing household.

How does solar work?

The technology that turns your house into a solar energy-harnessing hub is called photovoltaics, more commonly known as PV. PV works by fielding direct sunlight and absorbing its photons into the solar panels’ cells, which then creates electricity that provides energy for your home. This energy reduces your home’s output of carbon and other pollutants, which translates to cleaner air and water.

With the sun as the power source, the majority of the power generation occurs during the middle of the day, making summer the highest producing season. But don’t worry, it all evens out in the end.

Rooftop panels work best when they are exposed to sunlight, free of shade or shadow from nearby trees or structures. Given the sun’s east-to-west path, south-facing roofs are best-suited for maximizing your solar power. To see if your roof is set up for success, consult a mapping service or solar calculator to establish your roof’s suitability. If your roof isn’t up to standard, there are options such as ground mount solar installations and community solar gardens that you can explore.

Components

Solar panels: Capture the sun’s energy

Inverter: Converts the sun’s energy to a form that powers devices

Racking: The foundation that holds your solar system in place

Batteries: To store the energy generated

Charge controller: To control how quickly the batteries charge

What are the benefits of solar power?

Sustainability: Having a renewable source of energy coursing through your home reduces your household’s carbon footprint and increases your eco-friendliness.

Savings: How much money you save by going solar depends largely on how much energy your household consumes and the energy output of your solar panels. The cost of going solar has continued to decrease every year, so you are more likely to save as time goes on. For information on state incentives and tax breaks, explore what options apply to your home by visiting DSIRE (Database of State Incentives for Renewables & Efficiency).

Utilities: Whether your utility company charges a flat rate for electricity or charges variable rates throughout the day based on electricity production—i.e. higher rates in the afternoon, lower rates at night—solar power offsets the price you are charged for electricity. It becomes even more valuable during those higher-rate periods or during seasonal fluctuations in utilities costs.

Sell it back: Homeowners can sell their solar energy back to utilities through “Net-metering” plans. When your power generation rate is greater than your household’s consumption rate, the end result on your electric bill is a net energy consumption. Refer to DSIRE for region-specific regulations and policies.

Home value: A recent study by The Appraisal Journal found that homes with solar PV systems increased their sale price by an average of 3.74%, equaling a premium of $14,329.

Although the right solar solution looks different for each household, what remains true across the board are the environmental benefits and increased home values that solar power brings. Taking all this information into your research will improve your home’s renewable energy and reduce your carbon footprint.

The following analysis of the Southern California real estate market is provided by Windermere Real Estate Chief Economist Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact your Windermere agent.

ECONOMIC OVERVIEW

Employment levels across the Southern Californian counties contained in this report have been significantly impacted by the COVID-19-induced recession. Total employment in the region has dropped by a collective 1.99 million jobs between February and May of this year. With this massive contraction, it’s not surprising to see the unemployment rate rise from 4% in February to 17.6% in May. Unfortunately, as I write this, it appears as if infection rates in many California markets have increased significantly. As such, the likelihood of tangible increases in employment will be further delayed.

HOME SALES

In the second quarter of 2020, 33,614 homes sold. This was a drop of 32.6% compared to the same period in 2019. Sales were 2.5% lower than in the first quarter of the year.

If there is some solace in this report, it’s that pending home sales (an indicator of future closings) rose 6.4% over the first quarter of this year, suggesting that sales in the third quarter should pick up modestly from current levels.

Second quarter home sales activity dropped in all counties contained in this report. Of note was a significant decrease in Los Angeles County, where more than 6,600 fewer homes sold than a year ago.

There was an average of 26,957 homes for sale in the second quarter—down 32.4% from a year ago but 5.3% higher than in the first quarter of this year.

HOME PRICES

Year-over-year, the average home sale price in the region was $726,613. This was 0.6% higher than a year ago and 4.5% higher than in the first quarter of 2020.

Affordability concerns persist, which has had a negative effect on home price growth. Though prices did rise significantly between the first and second quarters, I wonder how much of this can be attributed—if even tangentially—to COVID-19.

Sale prices were higher in all counties contained in this report, with a significant increase of 6.5% in the more affordable Riverside County.

Conventional mortgage rates continue to break through historic lows and will remain that way for the foreseeable future. However, jumbo mortgage rates are still higher than we have seen in over a year. With higher rates, and tighter credit requirements, there will likely be ongoing impact on the counties with more expensive homes.

DAYS ON MARKET

It took an average of 35 days to sell a home in the second quarter, 10 fewer days than a year ago and 9 fewer days than in the first quarter of 2020.

All markets contained in this report saw the time it took to sell a house drop compared to the second quarter of 2019.

Homes in San Diego County continue to sell at a faster rate than other markets in the region. In the second quarter, it took an average of 23 days to sell a home there. This is 6 fewer days than a year ago.

Days on market shows that, although home sales are lower—a function of limited inventory levels—there still appears to be demand for homes when they do come on-line.

CONCLUSIONS

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

Although there is demand for homes, the renewed round of shutdowns could dampen that demand until infection rates level out and businesses reopen their doors.

The overall housing market is resilient but will likely not see significant growth until the state gets a handle on COVID-19. For that reason, I am holding the needle in the same position it was in the first quarter. It is still a seller’s market, but uncertainty persists.

ABOUT MATTHEW GARDNER

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

When considering downsizing your home, there are issues and stressors you may have never encountered. For seniors, this is a situation that sometimes comes from necessity.

And now, as the coronavirus pummels assets and incomes, downsizing may be more necessary for many as a way to reduce spending.

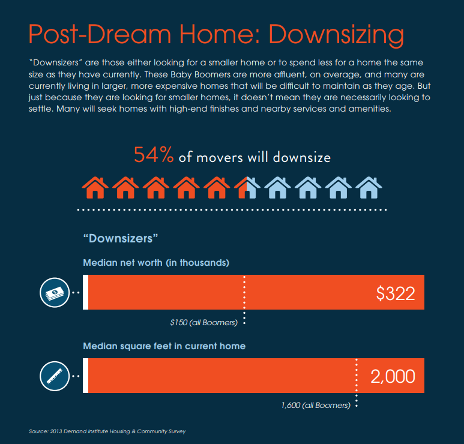

Already, as the number of baby boomers entering retirement continues to climb in the US, more people were considering downsizing than ever. And as many of these individuals have been empty nesters for years, some probably should have downsized already to save money.

Reasons for downsizing include:

Economic necessity.It’s common for many older adults to be faced with unexpected medical expenses, rising home insurance premiums and rising utility costs. Selling the house and moving into a more affordable space is often a solution.

Health concerns.Many seniors downsize to a home where at-home care is more available and there are fewer everyday obstacles to maintaining good health.

If you’re tired of doing all the housework that comes with a larger home, you’re not alone. A lot of retirees choose smaller homes where upkeep is less expensive.

An existing plan to relocate for retirement.Of those planning to move again for retirement, about half of those surveyed said they’d like to downsize. A projected 10 million retirees will downsize over the next decade.

Source: 2013 Demand Institute

Here are some key considerations for those thinking about downsizing:

Budgeting for a downsize

Choosing to downsize to a smaller home in retirement isn’t always motivated by economics but is always affected by it. Even for retirees in a high tax bracket, downsizing is often a goal for practical reasons. A smaller home, particularly in a multifamily building or development is far easier to maintain. This is a priority for people as they age and are less physically able to take care of a larger home.

Regardless of why you’re considering a new home, putting together a well-thought- out budget you can stick to is a wise first step. Some key considerations:

What are you paying now? What will you pay in a downsized home?

Make a list of all the expenses associated with your current home. This should include: mortgage payments, utility bills, maintenance costs, HOA fees, and everything else you pay on a monthly basis. You’ll be able to calculate these same expenses for your new, smaller home (or at least come up with a realistic estimate).

If you need to finance a downsized home, figure out the monthly mortgage payment for your new home, note its list price minus your down payment and plug that amount into Bankrate’s mortgage calculator. You’ll be able to change the mortgage term, down payment amount, and mortgage rate—giving you an idea of what your mortgage payment will be at the new home you’re considering.

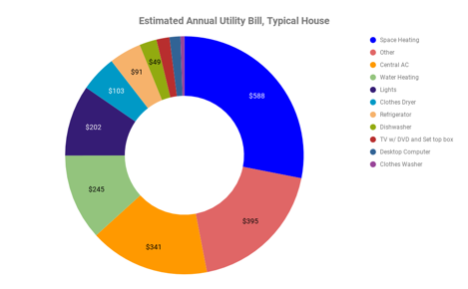

After coming up this number, you should also be able to determine a rough estimate for utility costs. If you’re thinking about moving out of state, take a look at the U.S. Energy Information Administration’s recent numbers for average monthly bills for single family homes by state. If you’re downsizing but also moving to a state where energy costs are on average higher, the savings may not be as great as you’d hoped. However, differences in energy costs can also work in your favor.

Let’s say you currently live in Connecticut, where average energy bills are among the highest in the nation–about $142 per month. If you move to Florida, where monthly energy bills are $123 on average, you’ll save a couple hundred dollars a year on energy alone.

Find out if your target home has an HOA with a monthly maintenance charge. Add these expenses up and the overall cost benefits of downsizing will become clear.

Source: 2016 Energy Star data

What’s your current income?

Preparing for a move is a great reason to reassess your financial big picture. Everyone’s financial outlook is unique, so taking the time to piece together all sources of income you have, as well as savings accounts and more, will help you develop a game plan.

Critical questions to ask yourself:

If you’re not yet retired, how realistic is your goal retirement date?

What will be your retirement income streams, and how much will these provide in monthly income?

Based on this income, how much home can you afford?

Do you have enough assets to afford a cash purchase?

What will it cost to sell your home and buy another?

Most retirees have been through the home-selling process before, but many haven’t in years, maybe decades. Take into account the extra fees and expenses that come into play when selling a home:

Realtor’s commission. The fee you’ll have to pay your realtor is typically 5-6% of the sale cost.

Closing costs. Depending on the real estate market you live in, you may be asked to take care of closing costs, which include property taxes, attorney fees, and other miscellaneous fees.

Inspections and home repairs. Buyers want thorough home inspections before signing on the dotted line; if any structural, electrical, or plumbing issues come up, you may have to cover those expenses.

Mortgage payoff. If your loan has a penalty for paying off the mortgage early, you’ll have an extra expense you may not have already accounted for. The sum you make from selling the home will mostly go into paying off the current mortgage.

The responsibility of some of these costs can shift from homeowner to homebuyer, so knowing exactly where you stand with these fees is a critical component to your downsizing budget.

Although there are many reasons for downsizing, budgeting carefully to make your new home less expensive than your current home is a huge benefit. It’s easy to lose track of all the small expenses that come with a move, but with a little diligence, you can save big in the long run.

What’s the plan?

Once your budget is in order, you’ll have to get the wheels turning on a strategy. There are a lot of moving parts in play, so breaking down your plan into simpler terms is a good place to start:

Will you use an agent or opt to sell the home yourself?

Keep in mind that selling the home yourself will entail a whole new list of responsibilities and tasks that may delay your moving process beyond your original timeline.

Will you be selling a car?

If you don’t do much driving, don’t want the responsibility, do want the money, or have a health concern keeping you from driving, selling a car is a wise decision. Many retired couples who have two cars and will sell at least one when downsizing as a way to collect some cash and free up space.

What other assets do you have?

A bittersweet, yet rewarding, part of downsizing is getting rid of stuff you no longer need. Whether that means valuables you no longer need or junk taking up space in your garage, let it go! You’ll be surprised at how freeing it is to clear out the basement and get paid for the stuff you haven’t used in ages.

Finding a place to live

Would you prefer to stay in the same area or are you excited about moving to a new place? If you’re moving somewhere new, take into consideration all the amenities you’ll need now and later on. Check for proximity to hospitals, grocery stores, and other essentials. Downsizing should make life easier—if you have to travel 45 mins to weekly doctor appointments, think about how that will affect your quality of life.

Considering all housing options

Single-family home — With a smaller single-family home, you can expect a similar lifestyle to the one you live now, but with fewer responsibilities and less clutter.

Condo/townhome — Condos and townhomes are excellent options for retired seniors who value their freedom and self-sufficiency and also want to get off the hook for property maintenance. Don’t forget to take a look at HOA fees.

Assisted-living community — Assisted living communities provide housing, meal prep, and health-related services for seniors. Many include luxurious amenities and a more thorough level personal care. Assisted living is an option for seniors with health concerns.

Move in with your adult children — If you’ll be living with family, any financial burdens you had in your own home will be eased. Being close to children and grandchildren is another benefit of moving in with family. Not enough room at their home? Do some research on “Granny Pods,” the latest trend in senior living. Granny Pods are essentially tiny homes that can be built in the backyard of your adult child’s home. Seniors who want to live with their kids can buy a Granny Pod and be close to home without feeling like a burden.

Finding a new mortgage

Downsizing to a new home in your retirement years puts you in a unique position when it comes to finding a mortgage.

After selling your old home and extra assets, you’ll be in a position to apply for a decent short-term mortgage with manageable monthly payments. Be sure to check mortgage rates often and track trends in your new area to secure the best loan you can. You’ll most likely be interested in one of the following:

10-year mortgage. The shortest-term mortgage and usually the one with the lowest rates, ten-year mortgages are great options for those who want to quickly accrue equity in their home and pay less interest than they would with a longer mortgage. Monthly payments will be higher than with other term-lengths, but if it is still lower than the payment you have at your current home, it’s worth it.

15-year mortgage. Fifteen-year terms will also carry lower mortgage rates and APRs than longer term mortgages, though obviously not as low as with a ten-year term. If you want to get the house paid off as quickly as possible but you aren’t comfortable with the monthly payment associated with a ten-year mortgage, consider a fifteen-year term instead. You’ll have a little more leeway in monthly spending while still paying off the home relatively quickly.

Reverse mortgage. If you want to tap into your current home’s equity before moving out, consider a reverse mortgage. Your bank will submit payments to you based on a percentage of the equity you have in your home and you won’t need to immediately pay it back. Loans don’t need to be paid back until the homeowner sells the home or dies, making reverse mortgages an intriguing retirement tool for seniors who are thinking about downsizing to a new home.

In times of uncertainty, one of the best things we can do to ease our fears is to educate ourselves with research, facts, and data. Digging into past experiences by reviewing historical trends and understanding the peaks and valleys of what’s come before us is one of the many ways we can confidently evaluate any situation. With concerns of a global recession on everyone’s minds today, it’s important to take an objective look at what has transpired over the years and how the housing market has successfully weathered these storms.

1. The Market Today Is Vastly Different from 2008

We all remember 2008. This is not 2008. Today’s market conditions are far from the time when housing was a key factor that triggered a recession. From easy-to-access mortgages to skyrocketing home price appreciation, a surplus of inventory, excessive equity-tapping, and more – we’re not where we were 12 years ago. None of those factors are in play today. Rest assured, housing is not a catalyst that could spiral us back to that time or place.

According to Danielle Hale, Chief Economist at Realtor.com, if there is a recession:

“It will be different than the Great Recession. Things unraveled pretty quickly, and then the recovery was pretty slow. I would expect this to be milder. There’s no dysfunction in the banking system, we don’t have many households who are overleveraged with their mortgage payments and are potentially in trouble.”

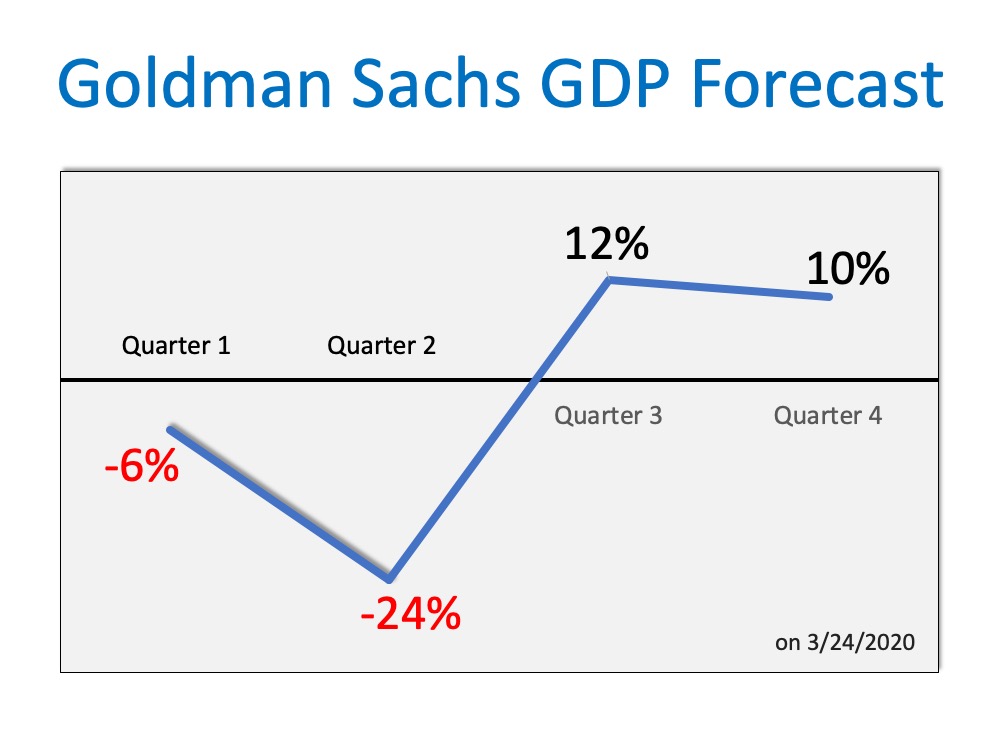

In addition, the Goldman Sachs GDP Forecast released this week indicates that although there is no growth anticipated immediately, gains are forecasted heading into the second half of this year and getting even stronger in early 2021.Both of these expert sources indicate this is a momentary event in time, not a collapse of the financial industry. It is a drop that will rebound quickly, a stark difference to the crash of 2008 that failed to get back to a sense of normal for almost four years. Although it poses plenty of near-term financial challenges, a potential recession this year is not a repeat of the long-term housing market crash we remember all too well.

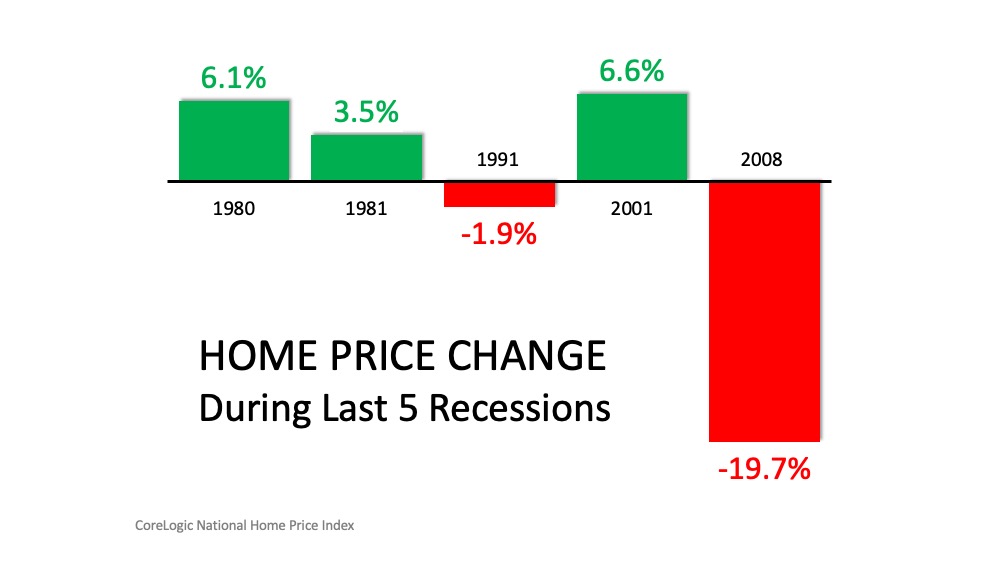

2. A Recession Does Not Equal a Housing Crisis

Next, take a look at the past five recessions in U.S. history. Home values actually appreciated in three of them. It is true that they sank by almost 20% during the last recession, but as we’ve identified above, 2008 presented different circumstances. In the four previous recessions, home values depreciated only once (by less than 2%). In the other three, residential real estate values increased by 3.5%, 6.1%, and 6.6% (see below):

3. We Can Be Confident About What We Know

Concerns about the global impact COVID-19 will have on the economy are real. And they’re scary, as the health and wellness of our friends, families, and loved ones are high on everyone’s emotional radar.

“Several economists made clear that the extent of the economic wreckage will depend on factors such as how long the virus lasts, whether governments will loosen fiscal policy enough and can markets avoid freezing up.”

That said, we can be confident that, while we don’t know the exact impact the virus will have on the housing market, we do know that housing isn’t the driver.

The reasons we move – marriage, children, job changes, retirement, etc. – are steadfast parts of life. As noted in a recent piece in the New York Times, “Everyone needs someplace to live.” That won’t change.

Bottom Line

Concerns about a recession are real, but housing isn’t the driver. If you have questions about what it means for your family’s homebuying or selling plans, let’s connect to discuss your needs.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

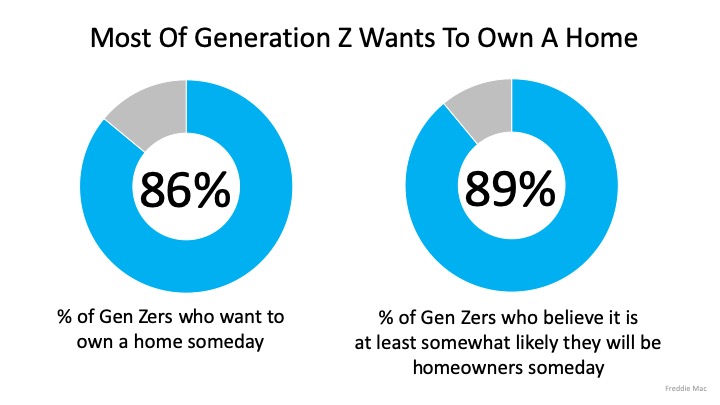

“The dream of homeownership is alive and well within “Generation Z,” the demographic cohort following Millennials.

Our survey…finds that Gen Z views homeownership as an important goal. They estimate that they will attain this goal by the time they turn 30 years old, three years younger than the current median homebuying age (33).”

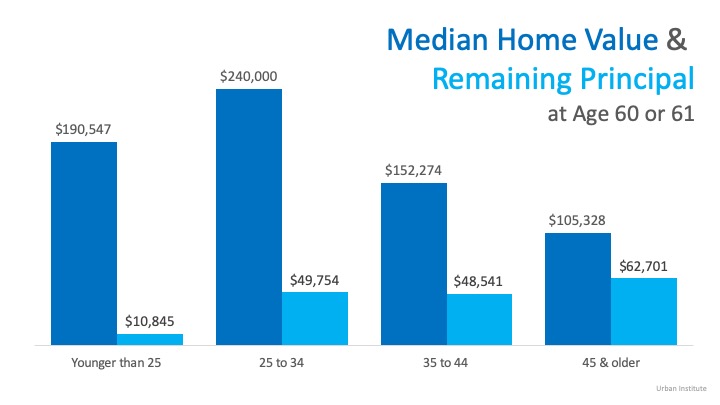

If these aspiring homeowners purchase at an early age, the Urban Institute study shows the impact it can have.

Based on this data, those who purchased their first homes when they were younger than 25 had an average of $10,000 left on their mortgage at age 60. The 50% of buyers who purchased in their mid-20s and early-30s had close to $50,000 left, but traditionally purchased more expensive homes.Although the vast majority of Gen Zers want to own a home and are somewhat confident in their future, “In terms of financial awareness, 65% of Gen Z respondents report that they are not confident in their knowledge of the mortgage process.”

Bottom Line

As the numbers show, you’re not alone. If you want to buy this year but you’re not sure where to start the process, let’s get together to help you understand the best steps to take from here.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors. As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

0 Comments

Comment